Annual Report 2009

- Corporate Social Responsibility Report

- Transparency and Rigor in Management

- Corporate Governance

In line with its commitment to transparency, managerial control and ethical conduct when engaging in business, Abengoa has opted for the following structure within its governing bodies:

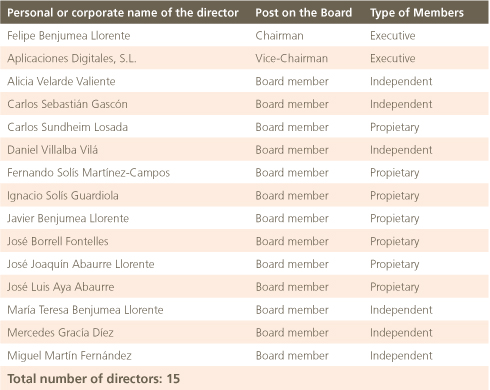

Board of Directors

Abengoa has devised its own Internal Regulations of the Board of Directors, by subjecting the actions of directors to a raft of rules on accepted conduct, guided by the principles of business ethics and geared towards upholding the priority of corporate interests, while ensuring the transparency “of financial, social, and legal information, among others, and the integrity of the resolutions adopted by the Board.

Membership of the Board of Directors is currently as follows:

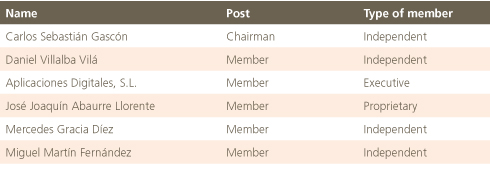

Audit Committee

As with the Board of Directors, and given the need for control mechanisms to function properly and efficiently, the Audit Committee is also subject to its own internal regulations.

Membership of the Audit Committee is currently as follows:

The Audit Committee primarily comprises non-executive members, thereby meeting the requirements prescribed by applicable law and regulations on good governance and, in particular, the Financial System Reform Act (Ley de Reforma del Sistema Financiero). Likewise, and in accordance with Article 2 of the Internal Regulations, the office of committee chairman must be vested in a non-executive member.

The duties and powers of the Audit Committee are as follows:

- Report on the annual accounts and half-yearly and quarterly financial statements that must be submitted to regulatory bodies and market monitoring bodies, making reference to the internal control systems, the control mechanisms to monitor implementation and compliance through internal audit procedures and, where appropriate, the accounting principles applied.

- Inform the Board of Directors of any changes in accounting principles, balance sheet risk and off-balance sheet risk.

- To report to the General Shareholders’ Meeting on those matters requested by shareholders that fall within its remit.

- To propose the appointment of the external financial auditors to the Board of Directors for subsequent referral on to the General Shareholders’ Meeting.

- To oversee the internal audit services. The Committee will have full access to the internal audit and will report during the process of selecting, appointing, renewing and removing the director thereof. It will likewise control the remuneration of the latter, and must provide information on the budget of the internal audit department.

- To be fully aware of the financial information reporting process and the company’s internal control systems.

- To liaise with the external audit firm in order to receive information on any matters that could jeopardize the latter’s independence and any others related to the financial auditing process.

- To summon those Board members it deems appropriate to its meetings, so that they may report to the extent that the Audit Committee deems fit.

- To prepare an annual report on the activities of the Audit Committee, which must be included as part of the annual accounts for the year in question.

- Supervise the preparation process and monitor the integrity of the financial information on the company and, if applicable, the group, and to verify compliance with regulatory requirements, the appropriate boundaries of the scope of consolidation and the correct application of accounting principles.

- Periodically review the internal control and risk management systems so that the principal risks are appropriately identified, managed and reported.

- Supervise the internal audit function, through full access to it, and monitor and supervise its independence and effectiveness; propose the selection, appointment, re-election and removal of the manager of the internal audit service; propose the budget for this service and set the remuneration for its manager; receive periodic information on its activities and the budget for the service; and verify that senior management takes into account the conclusions and recommendations of its reports.

- Establish and oversee a mechanism whereby employees may confidentially and anonymously, if deemed necessary, communicate potential irregularities, especially financial and accounting, which they may identify within the company, proposing the appropriate corrective measures and approvals to the Board of Directors.

- Submit proposals regarding the selection, appointment, re-appointment and replacement of the external auditor to the Board of Directors, including the terms of procurement.

- Receive regular information on the audit plan and the results of its implementation from the external auditor, and verify that the senior management takes the recommendations thereof into account.

- Safeguard the independence of the external auditor.

- Ensure that the group auditor is tasked with conducting the audits for the individual group companies.

- Oversee and resolve conflicts of interest. Pursuant to the Regulations of the Board of Directors, Board members are under the obligation to inform the Board of any situation of potential conflict, in advance, and to abstain until the committee has reached a decision.

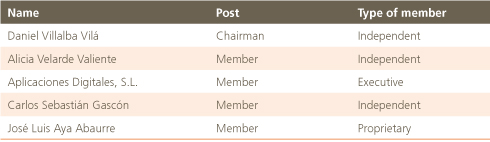

Appointments and Remuneration Committee

The structure and members of the Appointments and Remuneration Committee are as follows:

The Appointments and Remuneration Committee comprises a majority of non-executive directors. Likewise, in accordance with that envisaged in Article 2 of its Internal Regulations, the position of committee chairman must be held by a non-executive director.

The Appointments and Remuneration Committee is entrusted with the following functions and responsibilities:

- To report to the Board of Directors on appointments, reappointments, removals and the remuneration of the Board and its component posts, as well as on the general policy of remunerations and incentives for positions on the Board and within the senior management.

- To report, in advance, on all proposals that the Board of Directors presents to the General Shareholders’ Meeting regarding the appointment or removal of directors, even in cases of co-optation by the Board itself; to verify, on an annual basis, continuing compliance with the requirements governing appointments of directors and the nature or type thereof, all of this being information to be included in the Annual Report. The Appointments Committee will ensure that, when vacancies are filled, the selection procedures do not suffer from implicit bias that hinders the selection of female directors and that women who meet the required profile are included among the potential candidates.

- To prepare an annual report on the activities of the Appointments and Remuneration Committee, which must be included in the Management Report.

For further information on the structure and types of director and governing bodies, please consult the Annual Corporate Governance Report.

More information in Annual Corporate Governance Report

Photo taken by Adenilson Mendes de Lima, from Bioenergy, to the 1st Edition of the Abengoa Sustainability Photography Contest

Good Governance Practices

Following a favorable report from the committee, the full Board of Directors will approve the following company policies and strategies:

- Investment and financing policy

- Definition of the structure of the business group

- Corporate governance policy

- Corporate social responsibility policy

- Strategic or Business Plan, as well as the budget and management targets

- Remuneration and performance assessment policy for senior executives

- Risk control and management policy, as well as the periodic monitoring of internal information and control systems

- Dividends and treasury stock policy and, in particular, limits thereto

Case Study

Remuneration of Directors

Above and beyond the information required by law, Abengoa voluntarily included individualized breakdowns of the remuneration paid to each member of the Board of Directors, with figures for both 2008 and 2009.

The draft Sustainable Economy Act (Ley de Economía Sostenible), still awaiting enactment through the Spanish parliament, will require Spanish listed companies to include in their annual public information an individualized breakdown of the remuneration paid to directors, such obligation to take effect from the date on which the Act becomes law.

The company has therefore been voluntarily incorporating specific practices regarding good governance and transparent information reporting before they actually become obligatory for listed companies, another prime example of this approach being the implementation of its Audit Committee in 2002.

For further information on the remuneration of the members of the company’s senior governing bodies, please consult the Annual Corporate Governance Report.

2009 Milestones

- Reduction in the number of executive directors to 13%.

- Increase in the number of independent directors to 40%.

Transparent Practices

One of the cornerstones of the company’s strategy is its unflinching commitment to transparency and rigor. To reflect and strengthen this undertaking, the company set itself an objective several years back to the effect that all the information that appears in the Annual Audit Report must have its corresponding external audit report.

Therefore, 2007 witnessed the first audit of the company’s Corporate Social Responsibility Report. In 2008, this was extended to the Greenhouse Gas Emissions Report and in 2009, the Corporate Governance Report underwent an external audit process.

The company is not content with a moderate assurance audit report pursuant to ISAE 3000 standards, but rather aims to continue migrating towards a type of reasonable assurance audit report, which represents the most stringent kind of assurance to which a company can aspire.

In 2009, the company commissioned no less than six reports from its external auditors, all of which form an integral part of the Annual Report:

- Audit report on the consolidated accounts of the group, in accordance with applicable law.

- Voluntary audit report on internal control compliance under PCAOB (Public Company Accounting Oversight Board) standards, pursuant to the requirements imposed by section 404 of the Sarbanes-Oxley Act (SOX).

- Voluntary reasonable assurance audit report on the Corporate Governance Report, with Abengoa being the first listed company in Spain to obtain a report of this nature.

- Voluntary reasonable assurance audit report on the Corporate Social Responsibility Report.

- Voluntary audit report on the Greenhouse Gas (GHG) Emissions Inventory.

- Voluntary audit report on the design of the Risk Management System pursuant to ISO 31000 standard.