This website uses third-party cookies to collect statistical information related to your navigation. If you continue to browse, we consider you accept this use. See more information on our cookies policy here.

Annual Report 2011

- Corporate Governance

- Annual Report on Corporate Governance

- Other informations of interest

If you consider that there is any material aspect or principle relating to the Corporate Governance practices followed by your company that has not been addressed in this report, indicate and explain below. Within this section, you may include any other information, clarification or detail related to the abovementioned sections of the report, to the extent that these are deemed relevant and not reiterative.

Dentro de este apartado podrá incluirse cualquier otra información, aclaración o matiz, relacionados con los anteriores apartados del informe, en la medida en que sean relevantes y no reiterativos.

First annex:

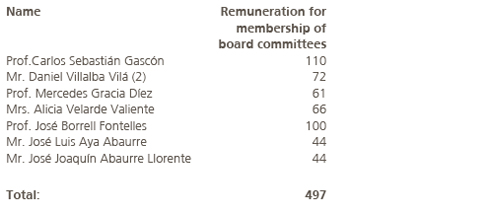

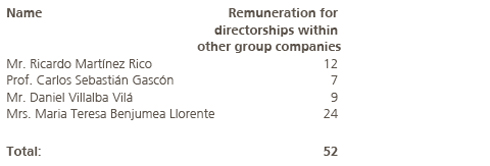

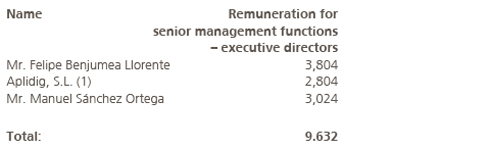

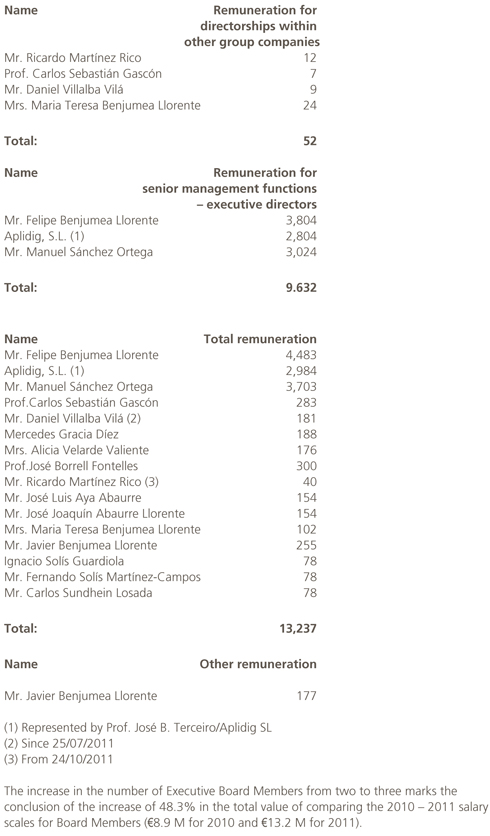

A table detailing the individual remuneration of directors is attached hereto as complementary information to section B.1.11 and following.

Remuneration of directors - 2011

(in thousand Euros)

Second annex

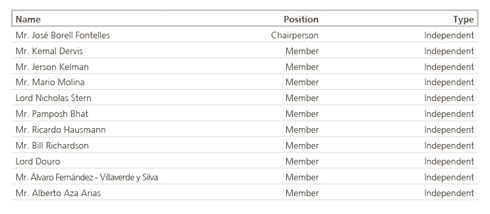

International Advisory Board

Abengoa on may 24,2010, created and International Advisory Board (IAB), and the Board of Directors as well as the chairman are responsible for its selection. The Secretary of the Board of Directors of Abengoa S.A acts as its Secretary.

The Advisory Board is a non-ruled voluntary body that renders technical and advisory consultancy services to the Board of Directors, to which it is organically and functionally subordinate, as consultant and strictly professional adviser. Its main function is to serve as support to the Board of Directors within the scope of it’s own competences, collaborating and advising, basically focusing its activities on responding to enquiries made by the Board of Directors in connection to all issues that the Board of Directors may enquire on or even raising proposals deemed outcome of their experience and analysis.

Its current composition is as follows:

Third annex

The Internal Code of Conduct in Stock Markets was instituted in August 1997 and it is applicable to all administrators, to the Strategy Committee members and to some employees depending on what they do and the information to which they may have access.

It establishes the obligation to safeguard the information and to protect the confidentiality of relevant facts prior to decision and publication, thus establishing the procedure for maintaining internal and external confidentiality, the ownership registration of shares, stock operations and conflicts of interests.

The Professional Code of Conduct was introduced in 2003, as a request from the Human Resources Management, and was modified in 2005 in order to add various elements that are common to the different companies that form Abengoa, bearing in mind their geographic, cultural and legal diversity. Said code gathers the fundamental values that must govern the actions of all the Company’s employees, regardless of their position or responsibility. The integrity of its behaviour, the strict observance of current legislation, its professional rigor, confidentiality and quality are part of Abengoa’s historical culture since it was set up in 1941 and still remain part of its corporate identity today.

The general secretary is responsible for follow-up and supervision. Available at www.abengoa.com

Fourth Annex

Abengoa and its Business Units have been operating a whistleblower channel since 2007 pursuant to the requirements of the Sarbanes-Oxley Act, whereby interested parties may report possible irregularities, in accounting, auditing or internal controls of financial reporting, to the Audit Committee. A register is kept of all communications received in relation to the whistleblower, subject to the necessary guarantees of confidentiality, integrity and availability of the information. The Internal Audit team conducts an inquiry into each claim it receives.

In highly technical cases, the company secures the assistance of independent experts, thus ensuring at all times that it has the sufficient means of conducting a thorough investigation and guaranteeing sufficient levels of objectivity when performing the work.Quinto Adicional

Fifth Annex

Article 8 of Abengoa’s Bylaws regulates the different rights inherent in Class A and B shares.

The following can therefore be summarized:

Class A Shares

At the nominal value of one Euro (1) each, and in the condition as ordinary shares, Class A Shares, (“Class A Shares”) grant holders the rights established by Law and set forth in these Bylaws with the specifications outlined hereunder:

1. Voting Rights

Each Class A Share grants its holder one hundred (100) votes.

2. Pre-emptive and free allocation rights over new shares

3. Notwithstanding the stipulations in section 2 above, each Class A Share grants all other rights, including economic rights, acknowledged by Law and set forth in these bylaws and in the rights entailed therein as holders of the condition of partner.

Class B Shares

Class B Shares, at a nominal value of one hundredth of a Euro (€0.01) each, (“Class B Shares” and, together with Class A Shares, “Shares with Voting Rights”), grant holders the rights established by Law and set forth in these Bylaws with the specifications outlined hereunder:

1. Voting Rights

Each Class B Share grants its holder one (1) vote.

2. Pre-emptive and free allocation rights over new Class B shares with regards to the principle of proportionality between the number of shares and class A shares, those of Class B and those of class

C (if already issued previously) over the total number of shares of the company, previously stated in relation to class A shares, the pre-emptive and free allocation rights of class B shares shall solely be aimed at class B shares (or convertible or exchangeable bonds or debentures, warrants or other securities and instruments that grant subscription or acquisition rights). Capital increases using reserves or premiums obtained from the issuance of shares executed by increasing the nominal value of the shares issued, as the case may be, Class B shares as a whole shall be entitled to nominal value increase in a proportion similar to the total nominal value of the Class B shares in circulation at the time of the execution of the agreement it represents with regards to the Company’s stock capital represented by the class A shares and by the class B shares circulating at such time.

3. Rights of Redemption for class B Shares

In the event that offers are tendered and accepted for the acquisition of the company’s entire shares with voting rights, following which the offeror, together with the persons cooperating therewith, (i) manage to directly or indirectly acquire voting rights in the company amounting or equal to 30 percent, except if another person, individually or jointly together with the persons cooperating therewith, already held a percentage of voting rights equal to or above that of the offeror after the offer, or better still (ii) having acquired shareholding below 30 percent, appoints a number of board members who, united, as the case may be, with those already appointed previously, may represent more than half of the members of the Company’s Administrative organ, each class B shares holder shall be entitled to a redemption by the company in accordance with Article 501 of the Corporations Act, except if the holders of the class B shares had already held the rights to participate in this offer and that such shares may have been acquired in the same manner and under the same terms and conditions and, whatever the case may be, for the same consideration as that of holders of class A shares (each offer that meets the characteristics described above, an “Apparent Redemption”).

Specifically, indicate whether the company is subject to non-Spanish legislation with regard to corporate governance and, if so, include the information it is obliged to provide and which is different from that required in this report.

No

List any Independent Directors who maintain, or have maintained in the past, a relationship with the company, its significant shareholders or managers, when the significance or importance thereof would dictate that the directors in question are not considered independent pursuant to the definition thereof set forth in section 5 of the Unified Good Governance Code:

No

Date and signature:

This annual corporate governance report was approved by the company’s Board of Directors at its meeting held on:

23/02/2011

Indicate whether there were any directors who voted against or abstained in relation to the approval of this report.

No

Additional information that must be included in the Corporate Governance Annual Report pursuant to law 2/2011 of 4th March, of the Sustainable Economy act

1st Provide a list of securities not traded on the Community Stock Exchange, indicating, as the case may be, the various classes of shares and the rights and obligations inherent in each class of shares.

Not applicable. Abengoa has not issued securities that may not be traded on the community stock exchange.

2nd Outline all the rules and regulations applicable to the modification of the company’s bylaws.

In compliance with the stipulations of Articles 285 and following of the Corporations Act, hereinafter, L.S.C, it remains the prerogative of the General Assembly of Abengoa to decide on any changes in the bylaws, except on the aspects over which competence is solely and legally reserved for the Board of Directors.

The internal rules and regulations of Abengoa include detailed regulations that govern the competence of the Assembly on the aspect of changes in the bylaws. Articles 8 and 30 of the bylaws of Abengoa address the competence of the General Assembly on matters regarding changes in the bylaws. Like Article 11 of the General Assembly Regulations, Article 30 of the bylaws establishes a special quorum:

“In order for the Ordinary or the Extraordinary General Assembly to decide, in general, on implementing any changes in the Corporate Bylaws, the attendance of shareholders in person or by proxy of at least fifty percent of the subscribe capital with voting rights shall be necessary in the first call. The second call shall only require the attendance of twenty-five percent said capital. In the event of the attendance of holders of less than twenty-five percent of the subscribed capital with voting rights, decisions may only be taken with the favourable votes of two thirds of the capital present or represented in the Assembly”.

Article 8 of the Bylaws establish separate voting possibilities in cases of changes in the bylaws deemed detrimental to Class B or C shares; thus this would require, in addition to approval by a special quorum, approval by a majority of Class B shares if the intended changes may be detrimental to them or by the majority of Class C, then in circulation, if the intended changes may be detrimental to such kinds of shares.

3rd List any restrictions whatsoever on the transferability of securities and any restrictions on the voting rights.

Abengoa has not imposed any kinds of restrictions on voting rights. Regarding the restrictions on the transferability of securities, see point A.10 of the IAGC.

4th Give an explanation on the powers of the members of the Board of Directors and, in particular, in relation to the possibility of issuing or repurchasing shares.

See point B.1.6; B.1.21, E.8 of the IAGC.

5th Provide detailed information on significant agreements undersigned by the company becoming valid, whether modified or terminated if the control of the company changes through a hostile takeover bid, and its effects, except if revealing such information may be damaging to the company. This exception shall not be applicable if the company is under legal obligations to reveal such information.

The eventuality has not arisen.

6th Give detailed information on the agreements signed between the company and its administrators and managers or employees with compensation rights in the event of resignation or unlawful dismissal or if work relationship is abruptly halted as a result of a hostile takeover bid.

Abengoa is not party to specific agreements of this nature.

7th Risks control systems in relation with the process of issuing financial information.

See point B.1.32 and letter D of the IAGC.

© 2011 Abengoa. All rights reserved