Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 27.- Gross Cash Flows from Operating Activities

Note 27.- Gross Cash Flows from Operating Activities

IFRS’s, as applied by Abengoa since the 2005 financial period, and specifically the interpretation IFRIC 12 of the International Financial Reporting Interpretations Committee (IFRIC) on service concession arrangements, which states, among other matters, that the construction contracts associated with this type of activities should be treated in accordance with IAS 11 (see Notes 2.24 b and c).

In addition to the service concession arrangements, the company undertakes a series of projects based on the integrated product (see Notes 2.4 and 6), which have a series of characteristics, which makes them comparable to service concession arrangements, these projects are outside of the scope of interpretation IFRIC 12, which refers exclusively to service concession arrangements. Such projects are financed through the Non-Recourse Project Finance model, in which a company of the Group undertakes the construction of the asset under a contract with agreed prices and timetables, which is analysed by an independent expert who reviews the contractual terms and the amount of the construction contract, verifying that they are carried out in market conditions.

Consequently, the results obtained of these operations which are mentioned in the previous paragraph cannot be recognized as accrued result until the assets are amortised or the transfer to third parties is effected. As such, neither profits nor operating cash flows from operating activities obtained in the construction of this type of asset are recognised within the financial statements.

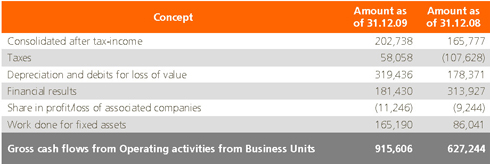

Without prejudice to international guidelines, and for the purpose of offering the users of Abengoa’s financial statements a fair view of the results and cash flows from operating activities, the Consolidated Cash Flows Statement as presented in these Financial Statements, includes the line Gross Cash Flow from Operating Activities which fairly reflects the cash flow generated from the operating activities, and whose details in financial years 2009 and 2008 were as follows:

The heading of work carried out for Fixed Assets reflects the balance of the net result to the construction contracts not subject to IFRIC 12 and the reversion of the amortization of the results attributable to such construction contracts which had previously been considered as an increase in the value of the asset.