Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 4.- Intangible Assets

Note 4.- Intangible Assets

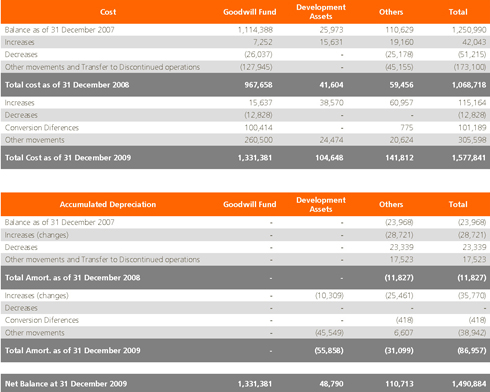

4.1. The following table sets out the movement in the main classes of intangible fixed assets between 2009 and 2008, analysed between those which are generated internally and other intangible assets:

“Other Movements” amounts generally reflect the transfer of assets in progress, changes in the consolidation perimeter, various reclassifications, exchange rate movements, and the transfer of assets held for sale relating to Information Technology business unit (see Note 14).

The most significant variations in the 2009 exercise generally occurred in the incorporation of the Goodwill (see Note 4.3.a) and of the intangible asset relating to the business segment of Information technologies previously classified as non-current assets held for sale, as well as in the increase in the Assets under Development relating to the Solar Business Segment activity (see Note 4.2).

These amounts relate only to Intangible Assets which do not relate to Project companies, an analysis of which is included in Note 6 on Intangible Assets in Projects.

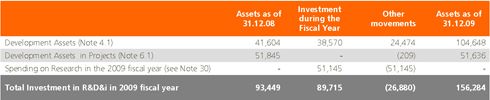

4.2. Assets under development

During the 2009 exercise, Abengoa has made significant R&D&I investment effects, investing a total of

€ 89,715 thousands through the development of new technologies in the various Business segments (Solar Technology, Biofuels, hydrogen, emissions management, energy efficiency and new renewables)

The following table summarises the total investments made in R&D in 2009:

The amounts for “Other Movements” generally reflect the variations of the perimeter of Consolidation and various reclassifications.

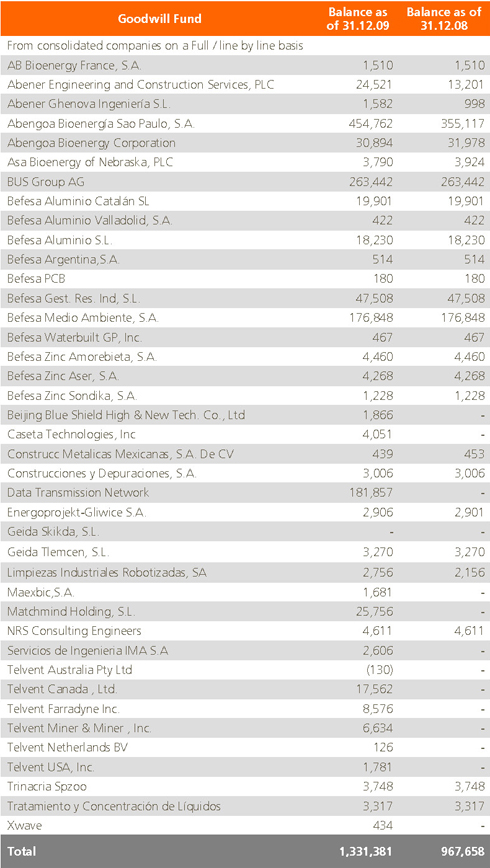

4.3. Goodwill

a) The table below shows the breakdown of Consolidation Goodwill by subsidiaries as of 31 December 2009 and 2008:

The most significant changes in the 2009 exercise mainly affect exchange rates caused by the appreciation of the Brazilian Real against the Euro and by the incorporation of the Goodwill for the Information Technologies business segment previously classified as non-current assets held for sale (see note 14).

Said Goodwill of the Information Technologies business segment must show what arose from the 2008 exercise acquisition of 100% of the DTN Holding Company Inc., a company belonging to Telvent GIT S.A., dedicated to providing business information services in the fields of Agriculture, Energy and the Environment, amongst others.

At the close of the 2009 exercise and pursuant to IFRS 3 on business combinations, the Administrators analyzed the assets and liabilities acquired and their subsequent assignment of their acquisition price for evaluation purposes, for which reason they considered the value of all the assets and liabilities, tangible and intangible, as well as contingent, as far as they may be objects of accounting recognition in accordance with the international accounting standards.

Thus, the assignment of the acquisition price entailed the consideration of all the factors taken into account when determining the acquisition price, the most important of which is the assignment of value (€ 160.4 M) to the intangibles associated with subscriber relationships, trademarks and IT applications (see Note 6.1).

On 31st December 2009, the difference between the acquisition price and the fair value of the assets and liabilities net acquired had been entirely assigned to goodwill as detailed below:

The variation between the previous amount and the recognized goodwill at the close of the exercise (€ 181,857 thousand) is completely a result of the conversion difference generated by the depreciation of the Dollar against the Euro.

b) As indicated in Note 2.7, Abengoa undertakes year-end procedures to identify potential goodwill

impairment.

The recoverable amount is the greater of its market value less related sales costs and its value in use, being the present value of estimated future cash flows.

To calculate the value in use of the major goodwill balances (Environmental Services, Bioenergy and Information Technologies), the following assumptions were made:

- Projected financial cash flows of the entity basis on the financial protections of the own Company at ten years, calculating a residual value based upon of the final year projected cash flow, but only on the basis that the cash flow of that final year fairly represents a normal flow for the business, in specific cases, applying a constant growth rate which in any case will be greater than that estimated for the market in which the entity operates.

- In main cases, the financial structuring of the entity is in some way linked to the global Group structure, a discount rate is utilised to calculate the present value of future cash flows based upon the weighted average cost of capital for that type of asset, with any necessary further adjustments if applies depending on the additional risk associated to some kind of activities.

- In any case, a further sensitivity analysis is performed, especially in relation to the discount rate, the constant growth rate, as the case may be, and the residual, with the objective to ensure that possible changes in the rates used do not impact on the possible recovery of the goodwill’s recorded carrying value.

- In applying these valuation criteria, the discount rates used to perform the impairment tests of the main Goodwill Funds (Environmental Services, Bioenergy and Information Technologies) were between 6% and 10%.

According to the usage value calculations, the hypothesis indicated above, no evidence has been found to show deteriorations in any of the main existing Goodwill Funds since the recoverable amount is greater than their net book value.

With regards to the remaining Goodwill amounts, as of the close of the period, the recoverable amount was estimated for Cash Generating Units (CGU) in accordance with Note 2.7 with there being no needed to recognise any impairment to such assets.