Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 11.- Derivative and Hedging Financial Instruments

Note 11.- Derivative and Hedging Financial Instruments

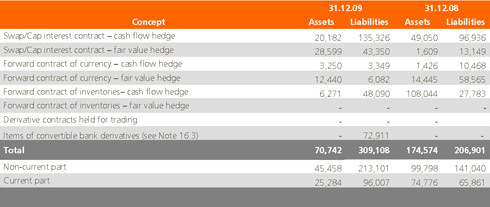

11.1. The fair value of financial instruments and hedging instruments held as of 31 December 2009 and 2008 was as follows:

The net amount of fair value transferred to the Income Statement of the 2009 and 2008 exercise for the derivative financial instruments designated as hedging instruments is € -2,512 and € -64,448 thousand respectively (see Note 23).

11.2. Foreign exchange hedging instruments

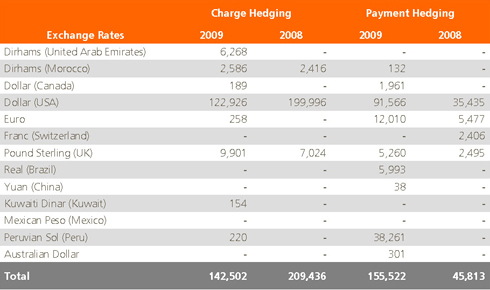

The following table shows a detail of the notional of the financial instruments as at the end of 2009 and 2008 relating to amounts receivable and outstanding in foreign currencies:

The following table shows the due dates of the covered notional by foreign exchange rate financial hedging instruments as at the end of 2009

At the close of 2009 and 2008 exercise, the fair value amount for the derivative financial instruments of the exchange rate directly recognized in the Income Statement because they fail to meet all the requirements specified by the IAS 39 that would enable its designation as hedging instrument is

€ -3,225 and € -53,576 thousand respectively (see Note 33).

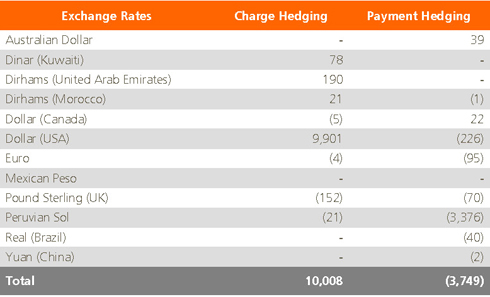

The table below is a detail of the maturity of notionals insured through financial instrument derivatives of exchange rate as at close of the 2009 exercise:

The table below is a detail of the maturity of the fair values of the financial instrument derivatives of exchange rate as at close of the 2009 exercise:

11.3. Interest rate hedges

As referred to in Note 9 of these Consolidated Annual Accounts, the general hedging policy for interest rate is to purchase future call options for a fixed fee through which the company can ensure a fixed maximum interest rate cost. Additionally, in certain circumstances, the company also uses interest rate swaps with variable to fixed interest rates.

As a result, the various hedging instruments and terms of such instruments, reflecting the characteristics and nature of the debt which carries the interest charge with the instruments are hedging, are somewhat diverse:

a) Loans with financial entities; between 74% and 100% of the notional, with loan terms up to 2017 with average interest rates guaranteed between 3.58% and 4.75% for loans pegged to the 1-month and 3-month Euribor rates.

b) Non-recourse financing;

b.1) Non-recourse financing in Euros; between 70% and 100% of the notional, including loan terms until 2032 with average interest rates guaranteed of between 2.00% and 5.25%.

b.2) Non-recourse financing in US Dollars; between 51% and 100% of the notional, including loan terms until 2023 with average interest rates guaranteed of between 5% and 8%.

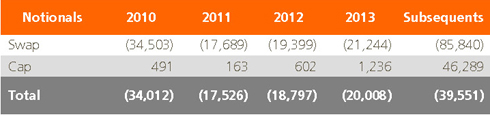

The table below shows a detail of the repayment schedule of the notional debt amounts covered by financial derivative instruments in the following 5 years:

The table below shows a detail of the maturity of the fair values of the financial instrument derivatives of exchange rate in the following 5 years:

At the end of 2009 and 2008, the net amount of the fair value of interest rate derivatives charged directly to the Income Statement, as a result of not fulfilling all the requirements of IAS 39 to be deemed a hedging instrument, supposed a loss of € -1,601 and € -18,664 thousands respectively (see Note 32).

Additionally, a series of interest rate Swaps and Caps were liquidated in June and July, generating a positive cash balance upon liquidation of the same amount. These contracts had been designated to hedge cash flows as a result of respective test of effectiveness expired. As such, applying IAS 39, when the hedge is considered to be interrupted and when the transaction being covered continues to be probable, the adjustments made to the cover within reserves until the most recent date in which the cover was effective, will remain in reserves. This amount will be taken to the Income Statement to the extent that the hedged instrument impacts the Income Statement. In this case, the Income Statement was impacted by the financial costs of the loan being covered. Abengoa has opted, on the basis of the aforementioned, to charge to results the benefits generated and charged to reserves, following the “swaplet” method. “Swaplet” refers to each calculation period of interest rate swaps. This method is based upon the principle that the balance registered in reserves will be equivalent to the sum of the current values of the cash flows of each “swaplet” (that’s to say, the difference between the fixed and forward rate calculated for each “swaplet” as at the final date upon which the cover was effective, discounted to that date).

The balance calculated for each “swaplet” is registered in the Income Statement in the corresponding period of each “swaplet”. The net gain transferred from reserves to the Income Statement in the 2009 and 2008 exercises amount to € 4,799 and € 4,474 thousand respectively, pending transfer to results in the following periods to the amount of € 26,904 thousand.

Finally, during the 2009 exercise, the amount of the fair value of the derivatives of interests recognized in the Income Statement due to the interruption of hedging assignments reached up to € -16,098 thousand.

11.4. Inventory purchase price hedging

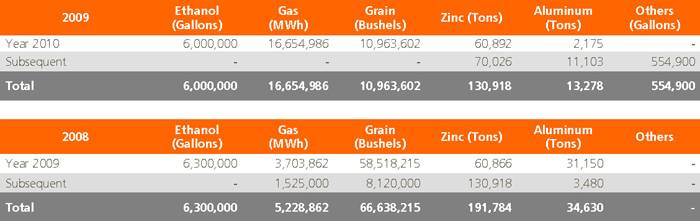

As indicated in Note 2.9 of these Abengoa accounts, the various activities of Abengoa through its various business groups (Bioenergy, Environmental services and Industrial engineering and construction) expose the group to various risks regarding the fair value of assets and raw material prices, primarily being zinc, aluminium, grain, ethanol and gas.

To hedge such risks, Abengoa uses futures contracts for both assets and purchases.

The following table shows the amounts covered and the maturities for the financial instruments of commodities for the closing period 2009 and 2008:

The table below is a detail of the fair value of the financial instrument derivatives from raw materials as at close of the 2009 exercise:

At the close of the 2009 and 2008 exercise, the amount of the fair value of the financial instrument derivatives of price of stocks directly recognized in the profit and loss accounts for failing to meet all the requirements specified by IAS 39 that would enable their designation as hedging instruments is -13,219 and € -1,267 thousand Euros respectively (see note 34).