Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 16.- Loans and Borrowings

Note 16.- Loans and Borrowings

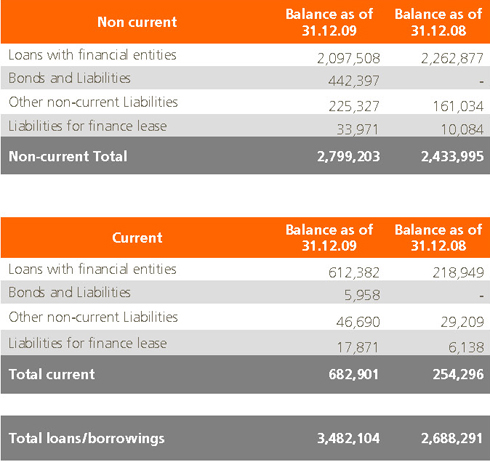

16.1. A detail of loans and borrowings as of 31 December 2009 and 2008 is as follows:

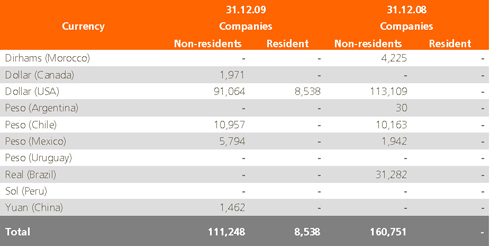

16.2. Loans and borrowings denominated in foreign currencies

a) The amount of loans with current and non-current credit entities includes debts denominated in foreign currencies in the amount of € 119,786 thousand (€ 160,751 thousand in 2008), out of which, € 111,248 thousand are for companies resident abroad and € 8,538 thousand to companies resident in Spain. The most significant value of exchange for currencies of debts in foreign currencies owed by companies of the Group to credit entities is as follows:

As in the prior year and with the purpose of minimising the impact interest rate volatility on these debts, certain hedging contracts have been entered into by the Group (see Note 11).

b) The following is a detail of loans with financial entities:

Like in previous exercises and with the aim of minimizing the volatility in interest rates of financial operations, specific contracts are signed to cover the possible variations that may occur (See Note 11).

The long term syndicated financing loans are raised for the purposes of financing investments and general financing requirements of the company, the first two of which are structured as lines of credit available to the Group, with the third being a multi-currency credit line. These loans are syndicated and financed by over 50 financial entities. The necessary individual guarantees have been provided by certain entities of the Industrial and Engineering Construction, Environmental Services and Bioenergy Business Groups.

The bilateral loans with the Official Credit Institute (ICO) and with Investment European Bank (BEI) are directed at financing specific investment programs, more notably overseas programs, and R&D programs.

Additionally, Abengoa, S.A. has available a total of € 170,550 thousand of short term borrowing facilities, of which € 162,976 thousand available as at the end of the period. These credit lines are primarily for financing short term working capital requirements of the Group, and are managed together with Group’s cash pooling arrangement (see Note 9 upon financial risk management).

The fair value of non-current third party loans is in line with the book value recorded, as the impact of discounting is not significant.

c) The debt repayment calendar is set out in the following table:

The exposure to the Group to movements in interest rates and the dates at which prices are revised is detailed in Note 9 upon the management of financial risks. The fair value of the current third party loans is equal their book value, as the impact of discounting is not significant. The fair value is based upon discounted cash flows, applying a discount rate being that of the third-party loan (see Note 11.3).

d) The balance of interest accrued which has yet to fall due is € 1,706 thousand as of 2009 (€ 3,967 thousand in 2008) which is included within “Short term debt with financial entities”.

e) Real estate pledged against mortgages as of 31 December 2009 is not significant.

f) The average interest rates associated with the debt facilities reflects normal levels in each of the regions and areas in which the facility was agreed.

Commitments and other loans

Convertible bonds

On 24th July 2009, Abengoa S.A. completed the process of issuing Convertible Bonds to qualified investors and institutions in Europe for the amount of € 200M including the right to exercise the option of increasing by € 50 M.

In summary, the final terms and conditions of the issuance are as follows:

a) The Bonds were issued for two hundred million Euros (€ 200,000,000) with maturity set to be in five (5) years.

b) The Bonds will accrue a fixed annual interest of 6.875% payable biannually.

c) The Bonds are exchangeable, at the choice of bondholders, for the Company’s existing shares.

Pursuant to the Terms and Conditions, the Company may decide to issue Company’s shares or give the combination of the nominal cash value with shares for the difference, in the event that investors decide to exercise their right of conversion.

d) The price of the initial exchange of the Bonds (Exchange Price) is twenty one Euros and twelve cents of a Euro (€ 21.12) for each share of the Company.

As defined in Note 2.18.1, and in accordance with what is set forth in the IAS 32 and 39, the fair value of the liability component of the convertible bonds as at 31st December 2009 amounts to € 187,717 thousand. In addition, the initial evaluation of the component of the liability implicit derivative generated in the issuance of the convertible bonds amounted to € 51,048 thousand and at the close of the 2009 exercise it was valued at € 72,911 thousand with an effect in the Income Statement of the 2009 (see Note 34) for the difference between the two previous values and which amounts to € -21,863 thousand.

Ordinary bonds

On 18th November 2009, Abengoa S.A. completed the process of issuing in Europe Convertible Bonds to qualified investors and institutions for the amount of € 250M, an amount that was increased up to € 300 M on 24th Novembre 2009 due to the existing additional demand.

In summary, the final terms and conditions of the issuance are as follows:

a) The Bonds were issued for three hundred million Euros (€ 300,000,000) with maturity set to be in five (5) years.

b) The Bonds will accrue a fixed annual interest of 9.625% payable biannually. Said interest rate may increase by 1.25% in the event that it does not obtain credit rating from at least two agencies 12 months after the aforementioned issuance.

16.4 Other loans

“Commitments and Other Loans” includes Sale and Lease back arrangements entered into by a subsidiary of Abengoa Bioenergy Corporation. These were:

- The Sale and Lease back of York’s facilities. The initial balance was for US$ 56.8 M agreed with

General Electric Capital Corporation (48.72%), and the Bank of America Leasing Corporation and Merrill Lynch Leasing (51.28%). The outstanding debt at the end of 2009 was US$ 24.1 M.

- Sale and Lease back of de Colwich’s facilities for $ 27.7 M, arranged with the Bank of America

Leasing Corporation (26.30%) and Merrill Lynch Leasing (73.70%). The debt outstanding at the end of 2009 was $ 16.6 M.

- Sale and Lease back of Portales’s facilities for $ 27 M arranged with GATX Financial Corporation. The outstanding debt at the end of 2009 was $ 17.2 M.

In accordance with the accounting treatment adopted, despite complying with the mathematical requirements of comparable standards and as well as criteria in relation to negotiations with the financial entities and despite having transferred 100% of the assets at these facilities, the assets in question remain within fixed assets on the consolidated balance sheet at their net book value.

Although, for operating purposes, the operation was undertaken through the ABC subsidiary, from a consolidated Group perspective the transactions imply the transfer of the asset and a commitment to make regular payments over a set period of time. In this sense, Abengoa is committed to future rental payments over five years (York), seven years (Colwich) and eight years (Portales) so as to continue operations within these premises, which represents an average annual charge of approximately $ 10 M (€ 7.2 M), as well as ensuring the maintenance of the plants in good operational condition and remaining as the plant operator should the purchase option not be exercised.

The entity has the option, albeit not obliged to exercise the option, to repurchase the facilities during a fixed period or at the end of the term at market price. If ABC or the Abengoa Group decides not to exercise the option, the Group is obliged to comply with a solution by the lessor in which the latter is able to dispose of or transfer the assets to third parties or another form of management.

The board are of the view that not treating these arrangements as financing leases represents a true and fair reflection of the substance of the arrangement and the financial position of the consolidated Group, taking into account the corporate strategy, the driving reasons behind the arrangements with the financial entities and, in particular, that there is no commitment to exercise the re-purchase option. In fact, the conditions of the transaction suggest there is in fact reasonable doubt as to whether such an option would in fact be exercises.

Additionally within “Commitments and Other Loans” are long and short term amounts payable to official entities (the Ministry of Industry and Energy, amongst others) relating to the repayment of loans and grants, without interest, provided for R&D projects. As of the end of 2009 such balances amounted to € 13,531 thousands (€ 10,263 thousands in 2008).

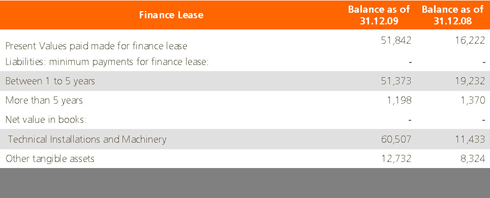

16.5. Financial Lease Liabilities

Finance lease creditors as at the end of 2009 and 2008 were: