Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 20.- Tax Situation

Note 20.- Tax Situation

20.1. Application of rules and tax groups in 2009

Abengoa, S.A. and 276 further Group companies (see Appendix V of these accounts) are taxed in 2009 under the Special number 2/97 Regime for Tax consolidation.

Telvent GIT, S.A. and 12 other companies (See Appendix V of these accounts) paid tax in 2009 under “Companies taxed under the Special Regimen for Tax consolidation number 231/05.

Similarly, Proyectos de Inversiones Medioambientales, S.L. and 11 further companies (see Appendix V of these accounts) are taxed in 2009 under the special regime 4/01B of the Basque country for Tax consolidation

Likewise, the 2009 exercise tax payment of Befesa Reciclaje de Residuos de Aluminio, S.L. and another company (see appendix V to this Report) fall under the Special Regime of Tax Consolidation of the Vizcaína Tax Regulation, with number 00109BSC.

The remaining Spanish and overseas companies that make up the Group are subject to corporation tax under the general tax regime.

The laws governing the Payment of Taxes on Companies within the Historical Territory of Vizcaya is that of Foral Law (Norma Foral) 3/1996 of 26th June, with the modifications incorporated by Foral Law 6/2007 of 27th March 2007, which is still valid although there are several appeals against it. In accordance with a ruling passed by the Court of Justice of the European Communities, the High Court of Justice of the Basque Country dismissed several appeals in December 2008 against the Foral Law on Company Taxation. Nevertheless, appeals have been filed at the Supreme Court against said decision. At the date of these financial statements, said appeals were still pending.

In order to calculate the taxable earnings of the consolidated tax Group and the individual entities which are within the consolidation perimeter, the accounting profit is adjusted to take into account the timing and permanent differences which may exist, giving rise to deferred tax assets and liabilities. Typically, deferred tax assets and liabilities arise as a result of making the valuations and accounting criteria and principles of the individual entities consistent with those of the consolidated Group, being those of the parent company.

The corporation tax payable, under the general regime or the special consolidated group regime, is the result of applying the applicable tax rate in force to each tax-paying entity, in accordance with the tax laws in force in the territory and/or country in which the entity is domiciled. Additionally, tax deductions and credits are available to certain entities, primarily relating to inter-company trades and tax treaties between various countries to prevent double taxation. Certain entities taxed under special regimes may receive given tax breaks and deductions due to the nature of their main commercial activity.

20.2. Deferred tax assets

With exportation as an integral element of its business, Abengoa, S.A. and various subsidiaries in Spain (belonging to the Industrial Engineering and Construction, Environmental Services, Bioenergy, Information Technologies and Solar business group) decided, in 2008, to reinitiate the application for tax benefits included in Article 37 of the Export Deductions (DAEX) of the Spanish Company Tax Law (LIS), for 2008 as well as previous periods that have not reached their expire date.

Despite the Export Activities Deduction (DAEX), for years, as a consideration with regards to investment decisions in certain projects, the Group, within the framework of tax position, did not consider it convenient to apply for such tax deductions (as done in 2001 and 2002), due to complications regarding the legal-taxation interpretations of the necessary requirements to be maintained so as to retain the rights described within said Article 37 of the LIS. For this reason, in certain cases, the Group chose to opt for alternative tax incentives for which the right to claim was not in question.

In the 2008 exercise, Abengoa deemed fit to carry out the deduction (DAEX), having met the conditions and requirements under which to apply the DAEX since in said exercise several Resolutions were published by the Tribunal Económico-Administrativo Central (central economic-administrative court, TEAC) sustaining the right to deduction by other groups of companies operating in environments and under circumstances similar to those of Abengoa, against the initial interpretation of the Public Tax Agency. Therefore, in the 2008 exercise the company did a comprehensive analysis of documents to back the right to the deduction, both for the 2008 tax period as well as for previous exercises that had not yet prescribed, for which the Group presented supplementary declarations for Company Tax based on the probability of an estimated recovery of those tax incentives.

Abengoa has re-estimated the probability of recuperating these tax incentives. As a consequence of this, the Group has included a deduction in its return to the amount of € 280 M (being both prior periods in which it was not applied for and the current period). However, due to tax planning requirements and taking into account the limit for the application of 10 years, as set out in the law, these fiscal benefits have still not been used through their reduction in quota of the Corporation Tax.

Considering the difficulty of the financial planning in the medium and long term in the present economic complex environment, as well as the complexity of its corresponding tax planning, the Group considers that, at this moment, and once taken into account the rest of the deductions and the applicable limits by the LIS, the recuperation of the tax credits could be probable to compensate in the amount of € 145 M, being this income recognised in the income statements of the current year results of € 18 M.

Regarding the accounting treatment of these reduction, both paragraph 4 of IAS 12 (which considers the accounting treatment corporate tax), as well as IAS 20 (which considers the accounting treatment of official grants in paragraph 2.b) exclude from their scope the accounting treatment of investment tax credits. In this sense, IAS 20.19 indicates the possibility that there exists the concept of a grant en certain tax packages with certain characteristics of an “investment tax credits” and recognises that on occasions it is complex to distinguish if the underlying components of an economic transaction are grants and what are their characteristics are.

The lack of specific guidance in either IAS 12 or IAS 20, regarding investment tax credits, makes it necessary for the Group to analyse on a case by case basis, the existing conditions so as to determine the appropriate accounting treatment in each event. From this analysis, the Group is of the view that there are cases in which the deduction is directly related to an investment in an asset, taking into account the concept of governmental assistance of the tax policy, thereby strengthening its character as a grant for accounting purposes. In this way, this treatment, considered as a grant, more reliably reflects the underlying economic attributes of the transaction. In such cases in which it is concluded, through an individual project by project basis, that the DAEX is a contributing factor in making the decision, of the investment, the Group registers the income in accordance with IAS 20, recognising such income as Other Operating Income. On the other hand, in those cases in which the aforementioned requirements are not met, the Group has considered that with regards to Art. 37 LIS it remains under IAS 12 and is registered as a tax on profits earned.

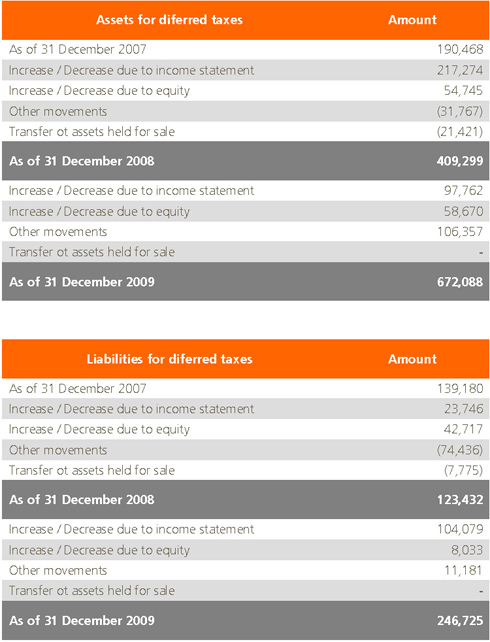

The movements in assets and liabilities between 2009 and 2008 due to deferred taxes were as follows:

With regards to assets held for sale (see Note 14).

The movement corresponding to the assets for deferred taxes charged to net equity during the 2009 and 2008 exercises basically corresponds to outcomes of the contracts of interest and exchange rate financial derivatives and raw materials for cash flow hedging operations.

The amounts stated in Other Movements for assets and liabilities of deferred taxes in the 2009 and 2008 exercises mostly correspond to the variations in the Consolidation Perimeter produced in said exercises, conversion differences, as well as the inclusion of deferred assets and liabilities relating to the business segment of Information Technologies previously classified as non-current assets held for sale for the approximate net amount of € 14 M (see Note 14).

The total balance of the assets for deferred taxes is basically tax credits for deductions yet to be taken with those generated by the outcomes of the contracts of interest, exchange and raw materials financial derivatives. Finally, it should be indicated that this amount includes assets for deferred taxes corresponding to deductions amounting to € 145 M for export-related activities by companies of the group in accordance with the valid laws.

The total balance of the liabilities for deferred taxes is, basically, with consolidation adjustments, business combinations (see Note 37) and applications of IFRS, basically through appreciation in applying the IFRS 1.

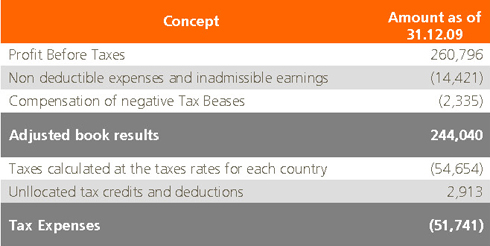

20.3. Tax on profit

A detail of the tax on profit in 2009 is as follows:

Tax on the Group’s earnings differs to the theoretical amount that would have been obtained by using the average weighted tax rate applicable to the consolidated profits of the Group. The difference arising between these two calculations in 2009 is set out in the following table:

The following may be highlighted amongst the reasons for such differences:

- The tax deductions earned through the efforts and dedication made to R&D&i activities: Abengoa’s efforts of investment in R&D&i over the last two years surpassed € 180 M. Most of these projects have obtained the motivated report by the Ministry of Science and Innovation in Spain (Ministerio de Ciencia e Innovación de España) with R+D qualification. The criteria followed for the accounting recognition of the R&D&i deductions involved considering it under the scope of IAS 12 and registering it on the line of profit tax since it fulfils all the prerequisites outlined in said standard regarding deductions in general.

- Tax deductions earned through export-related activities: the internationalization of Abengoa, through it investing in foreign companies with the clear intention of increasing the activities of exporting goods and services, meant the generation of a significant amount of tax deductions granted to export-related activities. The accounting criterion set forth in Note 20.2 is the one followed for the accounting recognition of the deductions granted for exporting activities.

- Contributions made to Abengoa’s profit from outcomes from other countries: 68.7% of Abengoa’s sales for the 2009 exercise are from countries other than Spain where tax rates are normally different. Also in the 2009 exercise, Abengoa obtained Outcomes from export-related and foreign project execution operations, which were subject to benefits from specific tax regimes.

- Taxation in Spain under the special regime of Tax Consolidation: Since 1997 most of the Abengoa companies that operate in Spain have paid taxes under the Tax Consolidation System which, amongst other things, allows the offsets of the tax-losses of subsidiary companies, higher tax deductions from the quotas for investments carried out in R&D&i and other activities, the deferment of taxes in operations occurring between companies of the same tax group which sometimes, depending on the operation, end up neutralizing the tax effect.