Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 2.- Summary of Key Accounting Policies

Note 2.- Summary of Key Accounting Policies

Below are set out the key accounting policies adopted in the preparation of Abengoa’s Consolidated Financial Statements.

2.1. Bases of presentation

The Consolidated Financial Statements for the year ending 31 December 2009 have been prepared in accordance with International Financial Reporting Standards (herein, IFRS), as adopted for use within the European Union.

Unless stated otherwise, the accounting policies as set out below have been applied consistently throughout all periods shown within these Consolidated Financial Statements.

The Consolidated Financial Statements have been prepared under the historical cost convention, with the exception of the revaluation of certain fixed assets in accordance with IFRS 1, and certain cases in which IFRS allow for the assets to be valued at its fair value.

The preparation of the Consolidated Financial Statements under IFRS requires the use of certain critical accounting estimates. It also requires that Management exercises its judgement in the process of applying Abengoa’s accounting policies. Note 3 provides further information on those areas which involved a greater degree of judgement or areas of complexity for which the assumptions or estimates made are significant to the financial statements.

The figures included within the schedules which together make up the Consolidated Financial Statements (Statement of Financial Position, Income Statement, Statement of Comprehensive Income, Statement of Changes in Equity, Cash Flow Statement and these notes herein) are, unless stated to the contrary, all expressed in thousands of Euros (€).

Unless stated otherwise, any percentage shareholdings shown include both direct and indirect ownership.

The IASB recently approved and published certain Accounting Standards, modifying the existing standards as well as IFRIC interpretations from which the Group adopted the following measures:

a) Standards, modifications and interpretations with validity date set as 1st January 2009 applied by the group:

- Modification to IFRS 2, “Share-based payments-conditions of irrevocability (or consolidation) of concession and cancellations".

-Modification to IFRS 7, “Financial Instruments: Disclosure”.

-Modifications to IAS 32 and to IAS 1, "Financial Instruments with put option and liabilities deriving from the liquidation.

-Modification to IAS 1, “Presentation of Financial statements”. The modification clarifies that the potential liquidation of a liability through the issuance of equity is relevant when classifying it as current or non-current.

-Modification to IAS 27, “Consolidated and Separate Financial Statements”.

-IAS 1 (Revised), "Presentation of financial statements" (valid from 1st January 2009 onwards). The revised standard prohibits the presentation of incomes and expenses (that is, “changes in non-proprietary net equity”) in the statement of changes in the net equity, requiring that such items be presented separately in an overall income statement statement. Consequently, the group presents all changes in the statement of changes in equity derivative transactions in the statement of changes that occurred in the consolidated net equity, such that all the changes in the non-proprietary net equity derivative transactions are shown in the overall income statement. The comparative information is re-stated in accordance with the revised standard. Since the modification only affects aspects of the presentation, there is no impact on the per-share profits.

-IAS 19 (Modification) “Employee Benefits” (valid from 1st January 2009 onwards).

-IAS 28 (Modification) “Investments in Associates” (and corresponding changes to IAS 32 “Financial Instruments: Disclosure”) (valid from 1st January 2009 onwards).

-IAS 39 (Modification) “Financial Instruments: Recognition and Measurement” (valid from 1st January 2009 onwards).

-Modification to IAS 38, “Intangible Assets”. The modification provides some patterns for evaluating the fair value of an intangible asset acquired in a business combination and allows the gathering of intangible assets in a single asset if each of them has a similar useful life.

-IFRIC 16 “Hedges of a Net Investment in a Foreign Operation” (valid from 1st October 2008 onwards).

-Modification to IAS 36, “Impairment of assets”. The modification clarifies that the largest cash-generating unit (or group of units) to which goodwill may be assigned for the purpose of impairment tests is an operative segment such as defined in paragraph 5 of IFRS 8, “Operating Segments”.

-Modification to IFRIC 9, “Reassessment of Embedded Derivatives”. This modification changes the scope paragraph to clarify that it is not applicable, in possible evaluations subsequent to the date of acquisition, of embedded derivatives in contracts acquired in a business combination between companies or businesses under common control or in the creation of a joint business.

-Modification to IFRIC 16, “Hedges of a net investment in a foreign operation”. The modification establishes that in the net investment of a foreign operation, the qualified hedging instruments may be maintained by an entity or entities within the group, which includes the very operation abroad, as long as the conditions of designation, documentation and effectiveness set forth in IAS 39 are met.

The application of these modifications and this revision bear no significant effect on the consolidated financial statements of the Group.

b) Standards, modifications and interpretations that have not yet become valid and which the Group has not adopted in advance:

At the date this consolidated financial statements were being prepared, the IASB and IFRIC had published the standards, modifications and interpretations outlined below and which are binding for the exercise starting as from 1st January 2010,

- IAS 27 (revised), “Consolidated and Separate Financial Statements”. The revised standard requires that the effects of all transactions with non-dominant shares be registered in the equity if no change occurs in the control, such that these transactions cease to give rise to goodwill or profit and/or loss. The standard also establishes an accounting procedure applicable in the event control is lost. Any remaining share kept in the company must be re-evaluated at its fair value, and a profit or loss entered in the outcome.

- IFRS 3 (revised), “Business combinations”. The revised standard retains the method of acquisition of business combinations, although it introduces significant changes. For example, all payments made for the acquisition of a business are entered at its fair value on the date of the acquisition, and the contingent payments which are classified as liabilities are evaluated on each date of close at the fair value, registering the changes in the outcome or income statement. It introduces an accounting policy option, applicable during each business combination, consisting of evaluating the non-dominant shares at their fair value or at the amount proportional to the net assets and liabilities of the acquired. All costs of the transaction are applied to expenses.

- IFRIC 17, “Distribution of non-cash assets to owners”. This interpretation sets patterns for entering agreements by virtue of which a company may distributes non-cash assets to its owners, such as distribution of reserves or dividends.

- IFRIC 18, “Transfer of assets from customers” (valid for financial years starting on 1st July 2009). This interpretation provides a guide on how to account for elements of fixed assets received from clients, or cash received and then used to acquire or create some specific assets. This interpretation is only applicable to assets used to connect the client to a network or to provide it a continuous access or an offer of goods or services, or for both.

- Modification to IFRS 2, “Share-based Payments”. This modification confirms that, in addition to the business combinations defined by IFRS 3 (revised), “Business Combinations”, contributions of a business in the creation of a joint business and transactions under common control are excluded from IFRS 2. (Applicable in yearly financial exercises starting on 1st January 2010).

- IFRIC 15 “Agreements for the Construction of Real State” (valid from 1st January 2010 onwards)

- IFRS 5 (Modification), “Non-current Assets held for sale and discontinued operations” (and corresponding modification to IFRS 1 “First-time Adoption of International Financial Reporting Standards”) (valid from 1st July 2009 onwards).

- IAS 32 (Modification) “Classification of Rights Emissions” (applicable in yearly financial exercises starting on 1st February 2010).

- IFRIC 12 “Service Rendering Agreements” (valid from 1st January 2010 onwards). This interpretation affects public-private service concession agreements if the grantor regulates the services to which the grantee must assign the infrastructure, to whom the services must be rendered and at what price, and if it controls any significant residual shares in the infrastructure at the time the agreement expires. The Group will apply the IFRIC 12 from 1st January 2010 onwards.

2.2. Principles of consolidation

With the objective of providing information on a consistent basis, the same principles and standards as applied to the parent company have been applied to all other entities.

All subsidiaries, associates and joint ventures included within the Consolidation Perimeter that forms the basis of these 2009 (2008) consolidated financial statements are set out in Appendixes I (VI), II (VII) and III (VIII), respectively.

a) Subsidiaries

Subsidiaries are those entities over which Abengoa has the power to control and implement financial and operational policy to obtain benefits from their operations.

It shall be assumed that a company has control if it directly or indirectly (through other subsidiaries) holds more than half of the voting rights of another company, except in exceptional circumstances in which it may be clearly demonstrated that such possession does not entail control.

Control shall also be said to exist if a company holds half or less of the voting rights of another and holds the following:

-power over more than half of the voting rights, by virtue of an agreement with other investors;

-power to manage the financial and operation policies of the company, by virtue of a legal provision, a bylaw or some kind of agreement with the aim of obtaining benefit from operations;

-power to appoint or dismiss the majority of the members of the board of administration or equivalent governing body that is actually in control of the company; or

-power to cast the majority of the votes in meetings of the board of administration or equivalent governing body that is actually in control of the company.

Subsidiaries are accounted for on a Full Consolidation Basis as of the date upon which control was transferred to the Group, and are excluded from the consolidation as of the date upon which control ceases to exist.

The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. The cost of acquisition is measured as the fair value of the assets given, equity instruments issued and liabilities incurred or assumed at the date of exchange, plus costs directly attributable to the acquisition. The excess of cost of the acquisition over the fair value of the Group’s share of the identifiable net assets acquired is recorded as goodwill. If the cost of acquisition is less than the fair value of the net assets acquired, the difference is recognised directly within the Income Statement.

Intercompany transactions and unrealised gains are eliminated and deferred until such gains are realised by the Group, typically in both cases via third party transactions.

Intercompany balances between entities of the Group included within the Consolidation Perimeter are eliminated during the consolidation process.

Appendix I and VI of these accounts identifies the 63 and 90 subsidiaries which were included within the consolidation in 2009 and 2008, respectively.

The following table shows those subsidiaries which during 2009 and 2008 were no longer included within the Consolidation Perimeter:

The sales and outcome contribution to the consolidated figures for the 2009 and 2008 exercises of companies that are no longer part of the Consolidation Perimeter were not significant.

On 27th May 2009, Abengoa S.A., through its subsidiary company, Telvent Corporation, executed a sales agreement for the sale of 3,576,470 ordinary shares of the company traded on NASDAQ, Telvent GIT S.A., representing 10.49% of the stock, amounting to a cash inflow of € 45M and an outcome of € 16.5M.

In addition to the above, on 28th October 2009, it executed another sales agreement for the sale of 4,192,374 ordinary shares, representing 12.30 % of the stock belonging to Telvent GIT S.A., amounting to a cash inflow of € 74M and an outcome of € 39.8M.

Upon the conclusion of the two aforementioned sales operations, Abengoa, S.A. now holds 40% of the stockshares in Telvent GIT, S.A. as at the time of the close of the 2009 exercise. It remains the main shareholder with full de facto control over said company consolidated by total integration consequence of the framework of the relationship existing between Abengoa S.A. and Telvent GIT S.A. through which it is availed the power to direct the financial and operation policies of Telvent with the aim of obtaining benefits from its activities such as set forth in IAS 27. Among the evidence obtained in the inclusion the following can be stated:

- the substantial control in management systems and control of the Company;

- that there be Shareholder Agreements that show evidence and ratify Abengoa’s support to the proposal as consequence of the exercise of "de facto control" over the company.

- the profile and degree of market activity of the other reference investors of the company in question, as well as of the shares transactions of said investors and the statements and communiqués from the reference shareholders on their intention to not take control of the company;

- the company’s free float, daily business volume of shares and on the % of shares held by Abengoa.

- the absence of agreements/pacts between other shareholders.

- the behaviour aligned with Abengoa of the other investors in the company’s Shareholders Assembly;

- the composition of the Board of Administration and analysis of its voting results.

- the structure of financing and guarantees that Abengoa provides to the company.

- etc.

On the other hand, and in June 2009, a company reorganization process within the Aluminium business belonging to the environmental services business group culminated into the simplified merger of the companies, Befesa Aluminio Bilbao (doing the takeover), Befesa Aluminio Valladolid (taken over), Aluminio Catalán (taken over) and Alugreen (taken over). The new company that emerged from said merger changed its corporate name to Befesa Aluminio, S.L. but retained the corporate address and CIF (Tax identification code) of the company that did the takeover, Befesa Aluminio Bilbao, S.L.

b) Associates

Associates are entities over which Abengoa has a significant influence but does not have control, which typically consists of a shareholding which represents between 20% and 50% of the voting rights. Investments in associates are accounted for using the equity method of accounting and are initially recognised at cost. The investment by the Group in associates includes goodwill identified on acquisition (net of any accumulated impairment loss).

The share in Income Statement after the acquisition of the associate companies is recognized in the Income Statement and their participation in subsequent movements is recognized in reserves. The accumulated movements subsequent to the acquisition are adjusted against the book value of the investment. When the share in the losses of an associate company is equal to or higher than the holding itself, including any other uninsured accounts receivable, additional losses are not recognized unless there have been obligations or payments assumed or made on behalf of the associate company.

Gains between the Group and its associates are eliminated to the extent of the Group’s holding in the associate. Additionally, unrealised gains are eliminated, unless the transaction provides evidence of impairment to the asset being transferred. The accounting policies of the associates have been changed where necessary to ensure consistency with the policies adopted by the Group.

Appendices II and VII of these Accounts set out the details of 5 and 7 entities which in 2009 and 2008, respectively, entered the Consolidation Perimeter and have been consolidated applying the equity method.

The table below sets out those associate companies which ceased to be associates within the Consolidation Perimeter in 2009 and 2008:

The impact upon the Group consolidated results of entities leaving the Consolidation Perimeter as associates was not significant in either 2009 or 2008.

c) Joint business

Such arrangements reflect a minority holding in a company which is jointly managed and owned in an equal share by an Abengoa company as well as by third parties external to the Group. Such arrangements are based upon an agreement between all parties that no single investor exercises greater control over the management and policies of the jointly owned business than any other investing party. Holdings in joint business are consolidated under the equity accounting method.

The Group consolidates on a line by line basis the assets, liabilities, income and costs and cash flows of the jointly owned business with similar lines in the Group accounts.

The Group recognises its share of gains and losses arising from the sale of Group assets to the jointly owned business for the part of the other invested entities. In contrast, the Group does not recognise its participation in any gains and losses made by the jointly owned business as a result of the purchase of assets by a Group company from the jointly owned business until such assets have been realised through the final sale of such assets to a third party entity. Any losses from the transaction are recognised immediately if there is evidence of a reduction in the net realisable value of the current assets, or an impairment of its value. Where necessary, the accounting policies of the joint ventures are adapted so as to ensure consistency with those adopted by the Group.

Appendix III of these Notes to the Financial Statements identifies the 4 entities which in 2009 have been incorporated within the consolidation perimeter.

The incorporation of the rest of the businesses into the consolidation, in the 2009 exercise, did not amount to significant incidence on the overall consolidated figures of December 2009.

d) Joint Venture

Joint Ventures (or Temporary Associations of Companies (UTE) as they are referred to in Spain), are entities which, while are not legally separately identifiable, form a basis of collaboration between businesses over a period of time, determined or otherwise, for the provision of works, services or supplies.

The proportional element of the Financial Statement and UTE’s Income Statement are integrated within the Income Statement of the participating company in proportion to its interest in the joint venture.

The total sum of operational financing provided by Group companies to the 122 joint ventures excluded from the consolidation perimeter, is € 281 thousand (€ 144 thousand in 2008) and is included under “Financial Investments” within the consolidated balance sheet. The net operating profit of the joint ventures accounts for 0.32 % of the Group consolidated operating profit (0.41% in 2008). The net proportional aggregated earnings were € 2,163 thousand in 2009 (€ 1,533 thousand in 2008).

During 2009 a further 72 joint ventures have been incorporated within the perimeter which commenced their activity and/or have started to undertake a significant level of activity in 2009. Such joint ventures made up € 64,190 thousand of net turnover (€ 289,170 thousand in 2008).

During 2009 56 joint ventures ceased activity or have become insignificant with regards to overall Group activity levels. The net profit in 2009 of such ventures was € 19,797 thousand (

(€ 166,443 thousand in 2008).

e) Transactions and minority holdings

The Group applies the policy of considering transactions with minority shareholders as transactions with third parties. The holding of minority shareholdings entails gains and/or losses for the Group which are recognised within the income statement. The acquisition of minority interests generates goodwill, being the difference between the consideration paid and the proportion of the book value of the net assets acquired.

2.3. Tangible fixed assets

2.3.1. Presentation

For the purposes of preparing the Financial Statements, tangible fixed assets have been divided between the following categories:

a) Tangible fixed assets.

b) Tangible fixed assets in Projects.

a) Tangible fixed assets

This category includes tangible assets of companies or project companies which have been self-financed or financed through external arrangements facilities with recourse.

b) Tangible fixed assets in Projects

This category includes those tangible assets of companies or project companies which are financed through non-recourse project finance (for further details see Notes 2.4 and 6 on Fixed Assets in Projects).

2.3.2. Valuation

In general, items included within tangible fixed assets are valued at historical cost less depreciation and net impairment losses, with the exception of land, which is presented at cost less any impairment losses.

The historical cost includes all expenses directly attributable to the acquisition of fixed assets.

Subsequent costs are recorded in the fixed asset register against the asset’s carrying amount, or as a separate fixed asset only when it is probable that future economic benefits associated with that asset may be separately and reliably identified.

All other repairs and maintenance costs are charged to the income statement in the period in which they are incurred.

Group internal work is valued at the cost of work and is shown as ordinary income in the income statement of the company which undertook the work. Such gains are eliminated upon consolidation so as to arrive at the cost of acquisition of the asset. Net proceeds of production sold during the installation period are also capitalized.

In accordance with that established in the relevant accounting standard for construction projects which are carried out by the Group, financing expenses accrued during the construction phase are considered as an increase in the cost and value of the asset, both with regards to financing achieved specifically for each project, as well as non-project-specific third-party financing from financial entities. Such capitalisation of financing costs ceases at the moment in which, as a result of delays or inefficiencies, the process is either stopped or has a greater duration than initially planned.

Costs incurred during the construction period may also include gains or losses from foreign currency cash flow hedging instruments for the acquisition of fixed assets in foreign currency which have been transferred directly from reserves.

With regards to fixed asset investments upon land belonging to third parties, an initial estimate of the costs to dismantle the asset and to repair the land site to its original condition is also included within the book cost of the asset. Such costs are recorded at their net present value in accordance with IAS 37.

Real estate investments entail proprietary office buildings retained for the purpose of obtaining long-term incomes and which are not occupied by the Company. The elements included in this section are shown by the costs of their acquisition or production less their corresponding accumulated amortization and losses caused by deterioration suffered.

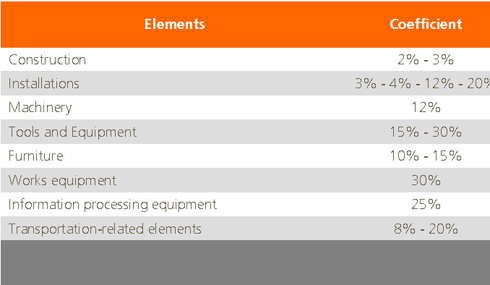

The annual depreciation rates of tangible fixed assets (including Fixed Assets Material in Projects) are as follows:

Secure waste deposits and similar assets are depreciated on the basis of the volume of waste in the deposit.

The assets’ residual values and useful economic lives are reviewed, and adjusted if necessary, at the close of the accounting period of the company which owns the asset.

When the book value of an asset is greater than its estimated realisable value, its value is reduced immediately to reflect the lower net realisable value.

Gains and losses upon the disposal of tangible fixed assets, calculated as proceeds received less the asset’s carrying net book value, are recognised in the Income Statement. Upon the disposal of re-valued assets, amounts recorded within the revaluation reserve are transferred to the profit and loss reserves.

2.4. Tangible fixed assets in projects

This category includes tangible and intangible fixed assets of companies within the Consolidation Perimeter for which their overall corporate objective is the development of an integrated product. Such projects are financed via Project Finance loans which are raised specifically and solely to finance individual projects as detailed in the terms of the loan agreement.

Integrated product development typically consists of the design, construction, financing, application of and maintenance of a Project (typically a large-scale complex operational asset such as a power station) which is owned by the company or is under concession for a period of time. The projects are initially financed through medium term bridging loans (typically being 2 years) and later via “Project Finance” loan agreements.

In this regard, the base of the finance agreement between the company and the bank lies in the allocation of the cash flows the project generates to the repayment of the financing and to satisfying the financial load, with exclusion or quantified payment of whatsoever other asset resource, in such a way that the recovery of the investment by the bank is exclusively through the cash flows of the project financed, with subordination to whatsoever other debt to which the non-Recourse Financing Applied to Projects is derived as long as the said finance has not been fully repaid.

Entities undertaking such projects may typically be in consortium with other third parties as well as an interests being held by Abengoa, S.A. or its subsidiaries.

Non-recourse project finance typically includes the following guarantees:

- Shares of the project developers are pledged;

- Assignment of collection rights;

- Limitations upon the availability of assets relating to the project.

- Compliance of debt coverage ratios

- Shareholders providing that these ratios are achieved.

On occasions, the shareholders hold an option to purchase the installations at a pre-agreed price, which is taken into account in determining the accounting treatment of the project. If considered necessary, a provision is made to reflect the difference in value between the net consolidated assets and the pre-agreed value of the purchase option, thereby avoiding the occurrence of losses in the event of the option being exercised.

Fixed assets in projects are valued depending upon their nature, with the following two types being considered:

- Tangible fixed assets: the remaining fixed asset belonging to the group entity undertaking the Project which do not fall within the parameters of the concession agreement.

- Intangible assets: assets assigned to companies under concession which, under IFRIC 12, are considered to be intangible. On this basis, there are a wide number of assets belonging to entities funded via Project Finance arrangements which may be classified as intangible assets within Project Fixed Assets.

Once the Project Finance has been cancelled or repaid, assets belonging to that entity are reclassified from Project Fixed Assets to tangible or intangible assets according to their nature on the consolidated balance sheet.

2.5. Intangible assets

a) Goodwill

Goodwill represents the excess of the cost of an acquisition over the fair value of the Group’s share of the net identifiable assets of the subsidiary or associate acquired at completion. Goodwill in relation to the acquisition of subsidiaries is included within Intangible Assets, while goodwill relating to associates is included within investments in associates.

Goodwill is carried at cost less accumulated impairment losses (see Note 2.7). Goodwill is allocated to Cash Generating Units (CGU) for the purposes of impairment testing; with CGU’s being units which are expected to benefit from the business combination which generated the Goodwill.

Gains and losses on disposal of an entity include the carrying amount of goodwill relating to the entity sold.

b) Computer programs

Program licences are capitalised as part of the cost base of the original program, being purchase costs and preparation/installation cost directly associated with the program. Such costs are depreciated over their estimated useful life. Development and maintenance costs are expensed to the income statement in the period in which they are incurred.

Costs directly related with the production of identifiable computer programmes adapted to the needs of the Group and which are likely to generate financial benefits that surpass the costs for over a period of one year are recognized as intangible assets if they fulfil the following conditions:

- It is technically possible to complete the production of intangible asset in a manner such that it may be available for use or sale;

- Management intends to complete the intangible asset in question, for its use or sale;

- The company is able to use or sell the intangible asset

- There is availability of appropriate technical, financial or other resources to complete the development and to use or sell the intangible asset; and

- Disbursements attributed to the intangible asset during its development may be reliably evaluated.

Costs directly related with the production of computer programmes recognized as intangible assets amortize during their useful lives estimated to be below 10 years.

Expenses that fail to meet the criteria above are recognized as expenses the very moment they are incurred.

c) Research and development costs

Research costs are generally recognised as an expense in the period in which they are incurred, analysing the cost between the various specific projects undertaken.

Development costs (relating to the design and testing of new and improved products) are recognised as an intangible asset when:

- It is likely the project will be successful (taking into account its technical and commercial viability).

- The costs of the project/product may be estimated in a reliable manner.

The capitalised costs are amortised once the product goes to market on a straight line basis over the period in which the product is expected to generate profits.

Any other development costs are recognised as an expense in the period in which they are incurred and are not recognised as an asset in later periods.

Amounts received as grants or subsidy loans to finance research and development are released to trading results on a percentage completion basis of the project which they part fund. Such monies are capitalised or expensed on the same basis as the project costs to which the funds relate.

d) Emission rights for own use

This heading recognizes greenhouse gas emissions allowances obtained by allocation for own use in the compensation with emissions while executing its production activities. The emission allowance acquired is valued at its cost of acquisition deregistering it from the balance sheet as a result of its delivery or of its expiry under the National Allocation Plan for the Allocation of Greenhouse Gas Emission Allowance.

Appropriate impairment tests are undertaken to establish whether the acquisition cost of the rights is greater than their fair value. If their fair value reduces, with the impairment being recognised in the financial statements, and their market value then subsequently recovers, it is also allowable to record the subsequent gain in the income statement, although the resultant carrying value may not be over and above the original cost of the rights.

Upon emitting greenhouse gases into the atmosphere, the Company provides for the tonnage of CO2 emitted at the average purchase price per tonne of rights acquired. Any emissions over and above the value of rights purchased in a given period will give rise to a remaining provision valued at the cost of such rights as at that time.

In the event that the emission allowance is not for own use but intended to be used for bargaining on the market the indications of note 2.12 will be strictly adhered.

2.6. Interest costs

Interest costs incurred upon the construction of any qualifying asset are capitalised throughout the period required to complete and prepare the asset for its intended use (at Abengoa a qualifying asset is defined as an asset for which the production or preparation phase is greater than one year).

Costs incurred relating to non-recourse factoring, when the accounting treatment requires the asset which being factored to no longer be recognised on the balance sheet, are expensed as costs at the point in which the factoring transaction is completed with the financial entity.

Remaining interest expenses are expensed in the period in which they are incurred.

2.7. Impairment of non-financial assets

At the close of each financial year, Abengoa reviews its non-current assets to identify any indications of impairment to the carrying book value. Additionally, at the end of each financial year, goodwill and other intangible assets which have not yet come into operation or have an indefinite useful life, are also reviewed to determine whether there has been any impairment to their carrying book value.

To establish if there has been any impairment to an asset’s carrying value it is necessary to calculate the asset’s recoverable amount. The recoverable amount is the greater of its market value less sales costs and value in use, being the current value of future cash flows generated by the asset. In the case that the asset does not generate cash flows independently to other assets, Abengoa calculates the recoverable amount of the cash generating unit to which the asset belongs. To calculate its value in use, the assumptions include a discount rate, growth rates and projected changes in both sales prices and costs. The discount rate is estimated by the directors, pre-tax, to reflect both changes in the value of money over time and the risks associated with the specific cash-generating unit. Growth rates and movements in prices and costs are projected based upon internal and industry projections and management experience.

In the event that the recoverable amount is less than the carrying value in the balance sheet, the corresponding impairment charge is made to “Impairment and Provisions” on the consolidated income statement. With the exception of Goodwill, impairment losses recognised in prior periods which are later deemed to have been recovered are charged as an income to the same income statement heading.

2.8. Financial Investments (short-term and long-term)

Financial investments are classified into the following categories, based primarily on the purpose for which they were acquired:

a) Financial assets at fair value with changes in the income statement;

b) Loans and receivables;

c) Financial assets held to maturity; and

d) Financial assets available for sale.

Management determines the classification of each financial asset upon initial recognition in the accounts, with their classification subsequently being reviewed at the close of each financial period.

a) Financial assets at fair value through profit and loss

This category includes the financial assets acquired for trading and those recorded at fair value with changes in results at the beginning. A financial asset is classified in this category if it is acquired mainly for the purpose of sale in the short term or if it is so designated by management. Financial derivates are also classified as acquired for trading unless they are regarded as hedges. The assets of this category are classified as current assets, except if they are held for trading or they are expected to be realized in more than 12 months after the closing date of the accounts of each company; in that case they are classified as non-current assets.

This are accounted for at fair value, not including transaction costs. Subsequent changes in fair value are accounted for in the income statement for the period.

b) Loans and accounts receivable

Loans and accounts receivable are considered to be non-derivative financial assets with fixed or determinable payments which are not quoted in an active market. They are included as current assets except in cases in which they mature more than 12 months from the balance sheet date.

In certain cases, and applying IFRIC Nº 12, there exist material assets under concession which are considered to be financial asset debtors (see Note 2.24.c).

These are initially recognised at fair value plus transaction costs, later depreciating the asset in accordance with the effective interest rate method. Interest calculated using the effective interest rate method is charged to the income statement under “Other Income”.

c) Financial assets held to maturity

This category includes those financial assets which are expected to be held to maturity and which and are not derivatives, with fixed or determinable payments.

These assets are initially recognised at fair value plus transaction costs, later recognising its repayment under the effective interest rate method. Interest expenses calculated under the effective interest rate method are charged to the income statement within “Other Income”.

d) Financial assets available for sale

This category includes non-derivative financial assets which do not fall within any of the previously mentioned categories. For Abengoa, these primarily comprise shareholding investments in other entities which do not fall within the consolidation perimeter. They are classed as non-current assets, unless management anticipates the disposal of such investments within 12 months following the date of the balance sheet being reported.

Financial investments are held at fair value plus transaction costs. Subsequent changes in fair value are recognised as changes in net reserves, with the exception of changes in conversion rates of monetary assets, which are charged to the income statement. Dividends from financial assets available for sale are recorded as “Other Income” in the income statement at the point at which the right to receive the income is established.

When financial assets available for sale are sold or are impacted by a fall in value or impairment, such changes in their fair value are recorded in the income statement. To establish whether the assets have been impaired, it is necessary to consider whether the reduction in its fair value is significantly below cost and whether it will be for a prolonged period of time. The accumulated loss is the difference between the acquisition cost and the current fair value less any impairment losses. In general, impairment losses recognised in the income statement are not later reversed through the income statement.

Acquisitions and disposals of financial assets are recognised on the date of trading, that is to say, the date upon which there is a commitment made to purchase or sell the asset. The investments are written off when the right to received cash flows from the investment has matured or has been transferred and when the Group no longer enjoys largely all risks and rewards associated with owning the financial asset.

The fair value of listed financial assets is based upon current purchase prices. If the market for a given financial asset is not active (and for assets which are not listed), the fair value is established using valuation techniques such as considering recent free market transactions between parties, reviewing the value of instruments of a substantially similar nature which have recently been traded, analysing the discounted cash flow of such assets and option price fixing models, using to the greatest extent possible, information available in the market.

At each balance sheet close it is considered whether there is any objective evidence as to whether the value of any financial asset or any group of financial assets has been impaired.

2.9. Derivative financial instruments and hedging activities

Derivatives are initially recognised at fair value on the date that the derivative contract is entered into, and are subsequently measured at fair value. The basis of recognising the resulting gain or loss depends upon whether the derivative is designed as a hedging instrument and, if so, the nature of the item being hedged.

The Group documents at the inception of the transaction the relationship between the hedging instrument and the item being hedged as well as its risk management objectives and strategy for undertaking various transactions. The Group also documents its assessment, both at hedge inception and on an ongoing basis, of whether the derivatives that are used in hedging transactions are highly effective in offsetting changes in the fair value of or cash flows of the hedged items.

On this basis there are three types of derivative:

a) A fair value hedge of recognised assets and liabilities

Changes in fair value are recorded in the income statement, together with any changes in the fair value of the asset or liability that is being hedged.

b) Cash flow hedge against anticipated transactions

The effective portion of a change in the fair value of derivatives is recognised in equity, whilst the gain or loss relating to the ineffective portion is recognised immediately in the income statement.

Accumulated amounts in equity are transferred to the income statement in periods in which the hedged item impacts profit and loss. However, when the forecast transaction which is hedged results in the recognition of a non-financial asset or liability, the gains and losses previously deferred in reserves are included in the initial measurement of the cost of the asset or liability.

When the instrument expires or is sold, or when the hedge instrument no longer meets the required criteria of a hedge, accumulated gains and losses recorded in reserves remain as such until the forecast transaction is ultimately recognised in the income statement. However, if it becomes unlikely that the forecast transaction will actually take place, the accumulated gains and losses in equity are recognised immediately in the Income Statement.

c) Net overseas investment hedging

Hedges of net investment in a foreign business operation, including the hedging of a monetary item considered part of a net investment, shall be entered in a similar way to cash flow hedges:

- The part of the loss or profit of the hedging instrument that is determined to be an efficient hedge shall be directly recognized in the net equity through the statement of changes in the net equity (see IAS 1); and

- The part that is inefficient shall be recognized in the Income Statement of the exercise.

The profit or loss of the hedging instrument in relation to the part of the hedge that is directly recognized in the net equity shall be entered under the outcome of the exercise at the time of the sale or disposition through another channel of the foreign business

The total fair value of hedging instruments is recorded as a non-current asset or liability when the hedged item is to mature in more than 12 months and as a current asset or liability if less than 12 months. Trading derivatives are classified as a current asset or liability.

Changes in the fair value of derivative instruments which do not qualify for hedge accounting are recognised immediately in the Income Statement.

Contracts held for the purposes of receiving or making payment of non-financial elements in accordance with expected purchases, sales or use of goods (own-use contracts) of the Group are not recognised as financial derivative instruments, but as executory contracts. In the event that such contracts include implicit derivatives, they are registered separately to the original contract, if the economic characteristic of the implicit derivative is not directly related to the economic characteristics of the original principle contract. The contracted options for the purchase or sale of non financial elements which may be cancelled through cash outflows are not considered to be “own-use contracts".

2.10. Fair value estimates

The fair value of commercial instruments which are traded on active markets (such as officially listed derivatives, investments acquired for trading and those instruments available for sale) is determined by the market value as at the balance sheet date.

The fair value of financial instruments which are not listed and do not have a readily available market value, is determined through applying various valuation techniques and through assumptions based upon market conditions as of the balance sheet date. For long-term debt the market price of similar instruments is applied. For the remaining financial instruments other techniques are used such as calculating the present value of future estimated cash flows. The fair value of interest rate exchanges is calculated as the present value of future estimated cash flows. The fair value of exchange rate contracts to mature at a future date are valued based upon market values as at the balance sheet date for similar products which mature at the same time.

The nominal value of accounts receivable and payable, less estimated credit adjustments are assumed to be similar to their fair value due to the short-term nature of the items. The fair value of financial liabilities is estimated as the present value of contracted future cash outflows applying the current market interest rate applicable to the Group were it to obtain a similar financial instrument.

Detailed information on the fair values is contained in the common note for all the financial instruments (see Note 9.2).

2.11. Inventory

Stock is stated, generally, at the lower of cost or net realizable value. In general, cost is determined by using the first-in-first-out (FIFO) method. The cost of finished goods and work in progress includes design costs, raw materials, direct labour, other direct costs and general manufacturing costs (assuming normal operating capacity). Interest costs are not included. The net realizable value is the estimated sales value in the normal course of business, less applicable variable selling costs.

Costs of inventories includes the transfer from reserves of gains and losses on qualifying cash flow hedging instruments relating to the purchase of raw materials, as is also the case for foreign exchange contracts.

2.12. Carbon emission credits (CER’s)

Various Abengoa´s entities are involved in a number of externally run schemes to reduce CO2 emissions through participation in Clean Development Mechanisms (CDM) and Joint Action (JA) programs with those countries/parties which are purchasing Carbon Emission Credits (CER’s) and Emission Reduction Credits (ERU’s), respectively. CDMs are projects in countries which are not required to reduce emission levels, whilst JA’s are aimed at developing countries which are required to reduce emissions.

Both projects are developed in two phases:

1. Development phase, which in turn has the following stages:

- Signing an ERPA agreement (Emission Reduction Purchase Agreement) which incurs certain related costs.

- PDD (Project Design Document) development.

- Obtaining certification from a qualified third party regarding the project being developed and submitting the certification to the United Nations where it remains registered.

Thus, the group currently holds various agreements for the rendering of consultancy services undersigned within the framework of the execution of Clean Development Mechanisms (CDM). Costs incurred in the rendering of said consultancy services are recognized by the group as long-term receivables.

2. Annual verification of reductions in CO2 emissions from which the company receives Carbon Emission Credits (CEC), which are registered at the National Register of Emission Rights. Its rights are treated as stocks and valued at its market value.

Furthermore, there are carbon fund holdings aimed at financing the acquisition of emissions from projects which contribute to a reduction in greenhouse gas emissions in developing countries through CDM’s and JA’s, as discussed above. Certain Abengoa companies have holdings in such carbon reduction funds which are managed by an external Fund Management team. The Fund directs the resources of the funds to purchasing Emission Reductions through MDL and AC projects.

The company with holdings in the fund incurs a number costs (ownership commissions, prepayments and purchases of CER’s). From the start, the holding is recorded [on the balance sheet] based upon the original Carbon Emission Credit (CER) allocation agreement, however this amount will be allocated over the life of the fund. The price of the CER is fixed for each ERPA. Based upon its percentage holding, and on the fixed Price of the CER, it receives a number of CER’s as obtained by the Fund from each project.

In both cases, both involvement in CDM and AJ projects and in the carbon funds, the CER is recorded as inventory by the company receiving the CER including, as an increase to book value, all costs incurred by the company in obtaining.

These contributions are considered as long-term investments and are recognized in the Balance Sheet asset under the heading of Other Financial Investments.

Likewise, the company may hold various Emission Allowances assigned by the competent EU Emission Allowance Authority (EUA) which may also be valued at their market price if held for their marketing. In the event that the EUA are held for purpose of own use, see note 2.5.

2.13. Biological assets

Abengoa recognises biological assets as tangible fixed assets, being sugar cane in production, from preparing the land to sowing the seedlings until the plant is ready for harvest and production. It is recognised at its fair value, being market value less estimated harvesting and transportation costs.

The agricultural products harvested from the biological assets, which in the case of Abengoa is cut sugar cane, is classified as inventory and is valued at the point of sale or at harvest based upon a reasonable estimated future sales value less expected sales costs.

The market value of biological assets and agricultural products typically used as a reference for the projected cane crop price in April is provided monthly by the Cane, Sugar and Alcohol Producers Board (Consecana).

Gains or losses arising as a result of changes in the fair value of such assets are recognised in the Income Statement.

According to the directors of the parent company, the assets are recorded at cost which is a reasonable approximation to its cost.

To obtain a fair valuation of the sugar cane, a number of assumptions and estimates have been made in relation to area of the farmed land, an estimated TRS (Total Recoverable Sugar contained within the cane) amount per ton to harvest the crop as well as the average amount of agricultural product growth in the various areas which are farmed.

2.14. Debtors and other trade accounts receivable

Trade receivables are recognised initially at fair value and subsequently are measured at amortised cost using the effective interest rate method less a provision for impairment. A provision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all amounts due as per the original terms of the receivables.

The amount of the provision is the difference between the asset carrying amount and the present value of estimated future cash flows discounted at the effective interest rate.

When a trade receivable is uncollectable, it is written off against the bad debt provision. The subsequent recovery of debts which were previously written off is credited against “selling and marketing costs” in the income statement.

Trade debtors and other accounts receivable which have been factored with financial entities are only removed from the Company’s accounting records and excluded from assets on the balance if all the conditions as required by IAS 39 have been met (See Note 9).

2.15. Cash and cash equivalents

Cash and cash equivalents include cash in hand, cash in bank and other short-term investments which are highly liquid in nature with an original term of three months or less.

On the Statement of Financial Position, bank overdrafts are classified as borrowing within short-term liabilities.

2.16. Parent company shares

The parent company shares are classified as net equity.

Additional costs directly attributable to issuing new shares are shown as a reduction, net of taxes, to the monies obtained from the issue. Any amounts received from the sale of own shares, net of costs, are included within reserves attributable to shareholders of the Parent Company.

2.17. Grants

Non-refundable capital grants are recognised at fair value when it is considered that there is a reasonable chance of the grant being collected and that the necessary qualifying conditions as agreed with the entity providing the grant will be adequately fulfilled.

Operating grants are deferred onto the Statement of Financial Position and are recognised in the Income Statement over the life of the costs to which the grant provides financial support.

Grants provided in relation to the acquisition of fixed assets are recorded as a reduction in the carrying value of the subsidised asset and are recognised in the profit and loss on a straight line basis over the estimated useful economic life of the subsidised asset.

2.18. Loans and borrowings

Loans and borrowings are initially recognised at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortised cost; any difference between the proceeds initially received (net of transaction costs incurred obtaining said proceeds) and the redemption value is recognised in the income statement over the period of the borrowing using the effective interest rate method.

Subsidised loans with no interest charge, granted for research and development projects, are not specifically covered by IFRS, making it possible to apply either IAS 20 or IAS 39. Abengoa considers such financial instruments as indicated in IAS 39.

Fees paid for obtaining credit lines are recognized as debt transaction costs as long as it is probable that a part or the entire credit line will be granted. In such a case the fees are differed until the granting occurs. Insofar as it becomes clear that part or the entire credit line may not be granted, the fees may be converted into an advance payment for liquidity services, thus amortizing it in the period of credit availability.

Loans and borrowings are classified as current liabilities unless an unconditional right exists to defer its repayment by at least 12 months following the balance sheet date.

2.18.1. Convertible bonds

On 24th July 2009, Abengoa S.A. completed the process of issuing Convertible Bonds to qualified investors and institutions for the amount of € 200 M which are due to mature within five (5) years.

Pursuant to the Terms and Conditions, Issuer may decide to issue Company’s shares or give the combination of the nominal cash value with shares for the difference, in the event that investors decide to exercise their right of exchange.

Following the stipulations of IAS 32 and 39 and in accordance with the Terms and Conditions of the issuance, since the bond grants the parties the right to choose the form of liquidation, the instrument gives rise to a financial liability. The right the contract grants to Abengoa to select the type of payment and with one of the possibilities of payment being the issuing of a varying number of shares and an amount of cash classifies the option of conversion as a liability embeded derivative. Thus, the instrument that emerges from the contract may be characterized as a hybrid instrument, which includes an element of liability for financial debt and a liability implicit derivative in relation to the conversion options held by the bondholder.

In the case of the convertible bonds that give rise to hybrid instruments, from the initial moment, the Company determines the value of said implicit derivative at a fair value and enters such value under the heading of liability derivative. At the close of each accounting session the value of the implicit derivative should be updated and the variations in the value should be entered through the Income Statement. The debt of the financial liability of the bond is calculated at the initial moment due to the difference between the nominal value received for said bonds and the value of the aforementioned implicit derivative. From then onwards said financial debt must be entered following the amortized cost method until its liquidation at the time of its conversion or maturity. The costs of the transactions are generally classified in the Balance Sheet as the lesser value of the debt, thus reverting as part of its amortized cost.

2.18.2 Ordinary bonds

On 24th November 2009, Abengoa S.A. completed a process of issuing Bonds to qualified investors and institutions for the amount of € 300 M which are due to mature within five (5) years.

From the very beginning the Company entered the financial debt at its net fair value, without any extra costs incurred in the transaction. This is followed by the application of the amortized cost method until its liquidation at the moment of its maturity. Any other difference between the net funds obtained (without any extra costs necessary for the obtaining process) and the value of reimbursement is recognized in the Income Statement Account during the existence of the debt. Ordinary bonds are classified as non-current liabilities except if they mature within the 12 months following the date of the Balance Sheet.

2.19. Current and deferred taxes

Tax amounts for the period comprise current and deferred taxes. Tax is recognised in the income statement, except to the extent that the tax relates to items recognised directly in reserves. In such a case, the tax cost/asset is also recorded directly in reserves.

The current income tax charge is calculated on the basis of relevant tax laws in force as of the date of the balance sheet in those countries in which the subsidiaries and associates operate and generate income which is subject to tax.

Deferred income tax is calculated, in accordance with the balance sheet liability method, based upon the temporary differences arising between the accounting treatment of assets and liabilities and the tax treatment assets and liabilities. However, deferred income tax is not accounted for if it arises from initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects either the accounting or taxation profit and loss. Deferred income tax is determined using tax rates and regulations which are enacted or coming into force at the balance sheet date and, as such, are expected to apply and/or be in force at the time when the deferred income tax liability is settled.

Deferred income tax assets are recognised only to the extent that it is probable that future taxable profit will be available against which the temporary differences may be utilised.

Deferred income tax is provided on temporary differences arising on investments in subsidiaries and associates, except where the timing of the reversal of the temporary difference is controlled by the Group, and it is likely that the temporary difference will not reverse in the foreseeable future.

As of 1/01/07 a variation in the Spanish corporation tax regulation was introduced relating to the corporate tax rate payable. The taxable rate in 2007 was 32.5% but and as of 2008, has changed to 30%.

As a result of this change, all Spanish companies (with the exception of companies registered and domiciled in the Basque Country) are subject to, and have applied, a corporation tax rate of 30% in 2009. Those domiciled in the Basque Country are subject to a corporation tax rate of 28% in 2009.

2.20. Employee remuneration and benefits

a) Share schemes

Certain Group companies are participating in a series of share-based incentive schemes for directors and employees. Such programs are linked to the achievement of certain agreed upon management objectives for the following years. When there is not an active market for the shares of the scheme, the proportional personnel cost is based upon the price identified in the scheme. In the case where the share price exists, the cost recognises as the quoted element of the fair value of the financial asset at the date of being granted. In either case, the impact of these share schemes upon the accounts of Abengoa is not significant.

Additionally, Abengoa, S.A. has implemented the following described share purchase plan for the Directors of the Group, which was approved by the board of directors as well as by shareholders at an extraordinary shareholder meeting on 16 October 2005:

- Available to: Up to 122 Abengoa directors (Directors of business groups, directors of business units, technical and R&D management and those responsible for corporate services) covering their subsidiaries and business groups, existing and future, which voluntarily wish to participate in the plan. The Plan is not applicable to any member of the Abengoa main board. The remuneration plan is linked to the achievement of certain management objectives.

- Number of shares: Up to 3,200,000 Abengoa shares, making up 3.53% of the share capital of the company.

- Those who benefit from the plan have been granted access to a bank loan facility, guaranteed by Abengoa and free of personal liability, for the purchase of Abengoa shares already in issue at market value, in accordance with the Stock Exchange rules, for an amount of € 87 million (including costs, commissions and interest). The repayment date of the loan is 7 August 2011. The plan sets out certain requirements to be achieved such as individual annual objectives for each director, as well as their continuation as an employee of the Group [during the course of the scheme].

Based on the specific conditions of the Plan, the operation is considered a transaction with payment in shares, settled in cash based on IFRS 2, by means of which the company acquires the services provided by the executives, incurring a liability for an amount based on the value of the shares.

The fair value of the executive services received in exchange for the granting of the option is recognized as a personnel expense. The total amount charged to expenses during the accrual period is determined by reference to the fair value of a hypothetical option to sell ("put") granted by the company to the executive, excluding the effect of the accrual conditions that are not market conditions, and included in the hypotheses on the number of options that it is expected will become exercisable. In this regard, the number of options it is expected will become exercisable is considered in the calculation. At close of each financial year, the company revises the estimation of the number of options it is expected will become exercisable and recognizes the impact of this revision of the original estimates, where appropriate, in the income statement

The fair value of options conceded during the year as calculated using the Black-Scholes valuation model was € 18,744 thousand (€ 30,021 in 2008). The key data required for the valuation model was share price, the estimated return per dividend, an expected option life of 5 years, an annual interest rate and share market volatility.

b) Bonus schemes

On 24 July 2006 and 11 December 2006 the main board of directors approved an extraordinary variable pay scheme for directors (Plan Two), as proposed by the Remuneration Committee. This plan includes 190 beneficiaries at a cost of € 51,630 thousand over a five year period from 2007 to 2011 and requires the achievement, on an individual level, of objectives as set out in the Strategic Plan as well as the individual’s continued ongoing service throughout the period of the plan.

In addition to that previously mentioned, and given that the acquisition of B.U.S. Group AB was completed only shortly following the establishment of the plan, on 22 October 2007 the main board of directors approved that the directors of B.U.S. Group AB (10 directors) will also enter the plan under the same conditions to a total amount of € 2,520 thousand.

The accounting treatment of this variable remuneration scheme is to recognise an annual cost in the income statement, being the creation of an accrual representing a percentage of completion of the objectives to be achieved [over the duration of the plan]. The expenses recognized during the exercise amounted to € 8,087 thousand, with the accumulated amount being € 21,566 thousand.

2.21. Provisions

Provisions are made when:

- There is a current obligation, being legal or substance, as a result of past events;

- There is more likelihood than not that there will be a future outflow of resources to settle the obligation; and

- The amount may be reliably estimated.

Where there are a number of similar obligations, the likelihood that there will be a required settlement is determined by considering the class of obligations as a whole. The provision is recognised even if the likelihood of an outflow with respect to any one item included within the same class of items is small.

Provisions are measured at the present value of the expected expenditure required to settle the obligation, recognising any increases in the provision over time as an interest expense.

Contingencies reflect possible obligations to third parties and known obligations which are not recognised due to the low probability of a future transfer of economic resources being required so as to settle the obligation or, that the potential future value of such a settlement cannot be reliably estimated. Such contingencies are not recognised on the balance sheet unless they have been derived from an onerous commitment in the context of a business combination. The balances disclosed in the notes to the accounts reflect the best estimate of the potential exposure as of the date of the accounts.

2.22. Suppliers and other payables

Trade payables are recognised initially at fair value and are subsequently valued at their amortised cost using the effective interest method.

Distributable income from advanced customer billing, as well as advances received from customers, are recognised as liabilities within “Other Liabilities”. This balance additionally includes grant income received which has yet to be charged to the income statement as of the balance sheet date.

2.23. Foreign currency denominated transactions

a) Functional currency

The components of the financial statements of each of the companies within the Group are valued and reported in the local currency as commonly used in that economic forum (the functional currency).

b) Transactions and balances

Transactions denominated in overseas currencies are translated into the functional currency applying the exchange rate in force at the time of the transaction. Gains and losses which arise upon later settlement of such transactions and upon translating monetary assets and liabilities upon the balance sheet which are denominated in foreign currencies are recognised in the profit and loss account. The exception is if the gains or losses are deferred to reserves as a result of a gain or loss arising from a qualifying hedging instrument.

c) Translation of the financial statements of overseas entities within the Group

The trading results and the balance sheet of all Group companies with a non-Euro (the Group reporting currency) denominated functional currency, are converted on the following basis:

1) All goods, rights and obligations are converted to the reporting currency using the exchange rate as at the closing date of the financial period, i.e. the balance sheet date of the companies within the Group.

2) The components of the income statement of each overseas entity are converted into the reporting currency using the average exchange rate of the period, calculated as the average exchange rates as of the close of the 12 monthly periods.

3) The difference between reserves, translated at historical rates, and net reserves resulting from the translation of the assets, rights and liabilities as per number “1)” above, is registered as a positive or negative adjustment, accordingly, to reserves under the heading “Exchange rate differences”.

The translation of the results of those entities within the Group which are consolidated using the equity accounting method, applies the average exchange rate for the period, as calculated in point “c.2” above.

Adjustments to goodwill and to fair values that arise upon acquiring an overseas entity are treated as assets and liabilities of the overseas entity and are translated at the closing balance sheet exchange rate.

2.24. Revenue recognition

a) Ordinary income

Ordinary income comprises the fair value of consideration received for the sale of goods or services excluding any related charges resulting from the operations, before any discounts or returns and excluding sales between Group entities.

Ordinary income is made up of the following:

- Income from the sale of goods is recognised upon the Group delivering of the product to the customer, the customer accepting the goods and that it is reasonably likely that the related account receivable will be received from the customer.

- Income from the sale of services is recognised in the period in which the service is provided, based upon the contractually agreed rates and the percentage of completion of the service being provided.

- Income from interest is recognized by using the effective interest rate method. When a account receivable undergoes loss through impairment, the book amount is reduced to its recoverable value, discounting estimated future cash flows at the original effective interest rate of the instrument and the discount is recorded as a reduction in interest income. Income from interest on loans that has undergone loss impairment is recognized when the cash is collected or on the basis of the recovery of the cost when the conditions are guaranteed.

- Dividend income is recognised when the right to receive payment is established.

b) Construction contracts

Costs incurred in relation to construction contracts are recognised at point in which they are incurred. When the eventual gain or loss of a construction project cannot be reliably estimated, revenues are only recognised up to the amount of the costs incurred to date, on the basis that such costs are anticipated to be recovered.

When the financial gain or loss of a construction project may be reliably estimated and it is likely that it will be profitable, income is recognised upon the contract throughout the period of the project. When it is probable that the costs of the project will be greater than the income, the full anticipated project loss is recognised immediately as a cost. To determine the appropriate amount of income to be recognised in any period, the percentage to completion method is applied. The percentage to completion method considers, at the balance sheet date, the actual costs incurred as a percentage of total anticipated costs for the entire contract. Costs incurred in the period which relate to future project activities are not included when establishing the percentage of completion. Prepayments and certain other assets are recognised as stock, depending upon their specific nature.

Invoices emitted yet to be received and customer retention payments are recorded within debtors and other trade receivables.

Gross amounts owed by clients for ongoing works in which the costs incurred plus recognized benefits (minus recognized losses) exceed partial invoicing are presented as assets in the heading of “clients, finished construction pending certification”.

In contrast, amounts outstanding from customers for work in progress for which the billing to date is greater than the level of costs incurred plus recognised gains (less losses recognised), are shown as a liability.

c) Concession contracts

Integrated Products (see Note 2.4) are long-term projects awarded to and undertaken by Abengoa’s entities (in conjunction with other companies or on an exclusive basis) typically over a term of 20 to 30 years. Such projects typically include both the construction phase of certain infrastructures as well as the provision of future associated maintenance services throughout the concession period.

Revenues are obtained during the concessional period via an annual charge payable by the body which granted the concession which, in certain cases, is adjusted for inflation. Typically the annual charge is updated based upon the official pricing index of the country and in the currency in which the cannon is denominated, with fluctuation in local currency being assessed against a currency basket.

In general, the accounting of this type of projects follows the interpretation of IFRIC Nº 12 Service Concession Agreements with assets constructed being treated as Intangible Assets (Concessions) as per the following criteria:

1) Total construction costs, including associated financing costs, are registered as a tangible asset. Profits attributable to the construction phase are recognised on a grade of completion basis, based upon the fair value assigned to the construction and the concession.

2) Upon completing the construction phase of the concession and entering the service phase, the construction costs are moved from tangible to intangible assets.

3) The intangible asset is amortised, in general, on a straight line basis over the period of the concession.

4) The charges to the Income Statement during the period of the concession are as follows:

- Ordinary income: The annual updated concession fee income is recognised each in period.

- Operating costs: operating and maintenance costs and general overheads and administrative costs are charged to the income statement in accordance with the nature of the cost incurred (amount due) in each period. Fixed assets are amortised as per point 3) above.

- Financial costs: Financing costs and exchange rate differences arising from debt repayable which is denominated in foreign currencies are charged to the income statement.

At the end of the period, each project is reviewed to determine whether it is necessary to recognise any impairment to its value due to the non-recuperation of costs, as long as the amount may be calculated.

However, in those cases where it is the responsibility of the party which granted the concession to make good the payment of the operator’s expenses and retain substantially all the risks associated with the concession requirements, the asset arising from the construction of phase of the project is reported as a long-term debtor as long as the amount may be calculated. The long-term debtor is gradually reduced during the life of the contract by matching against it the annual fees received from the customer.

2.25. Rental contracts

The leasing of fixed assets in which a group company is the lessee and substantially conserves all the risks and advantages resulting from the ownership of the assets is classified as financial leasing.

Finance leases are recognised upon entering into the contract at the lower of the fair value of the leased asset and the present value of the minimum leasing payment throughout the contract term. Each lease payment is analysed between debt and financing costs, in a way which establishes a constant rate of interest upon the outstanding debt at any time. The amounts to be paid throughout the lease term, net of financing charges, are recognised as long-term and short-term creditors, as appropriate. The implicit interest cost element of the rental payments is charged to the income statement throughout the period of the leasing agreement applied the implicit interest rate constantly throughout the contract to the remaining creditor on the balance sheet. Fixed assets capitalised through finance lease agreements are depreciated over the lower of the lease agreement term period or the anticipated useful economic life of the asset.

For leasing agreements undertaken by the Group in which the entity entering into the agreement does not substantially take on the risks and rewards of ownership are recorded as operating leases. Payments made under operating leases are charged to the income statement (net of any incentives received from the lessor) on a linear basis over the term of the contract.

2.26. Dividend distribution

Dividends paid to the shareholders of the parent company of the Group are recognised as a liability in the period in which the dividend payment is approved by the shareholders of the company.

2.27. Financial information by segment