Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 37.- Business Combinations

2009 Annual Consolidated Accounts

Note 37.- Business Combinations

- On 21st May 2009, Telvent Outsourcing, S.A, a subsidiary to Telvent GIT, S.A, parent company of the Business Group specialized in Information Technologies, reached an agreement for the acquisition of 42% remaining of the company called Matchmind in the hands of the executive team and one of its founding members for a total of € 18.8M as part of an original agreement reached in October 2007 on the acquisition of 58%.

Since the agreements for the acquisition of 42% of Matchmind were originally undersigned in October 2007, and pursuant to the stipulations of IFRS 3 on business combinations, the 31st October 2007 was admitted as the reference date of the actual acquisition of said percentage when determining the goodwill integrated in the consolidation perimeter in previous exercises.

Had it been part of the Group from 1st January 2009 onwards, the contribution of 42% of Matchmind would not have amounted to a very significant variation with regards to the consolidated results after taxes for the 2009 exercise. - On 2nd June 2009, the dependent company, MRH Residuos Metálicos, S.L., after creating two subsidiaries in Germany, Befesa Slazschlacke GmbH and Befesa Slazschlacke Sud, GMBH, acquired, for an amount of € 25.5 million, three productive plants located in the German towns of Hannover, Lünen and Töging, and specialized in the treatment and recycling of salt slag. They are equipped with the latest technology existing on the market, and with a combined treatment capacity of 380,000 tons of waste per year.

Said acquisitions did not mean the acquisition of the companies that were the previous owners of the aforementioned assets but their direct acquisition while maintaining the personnel affected by said assets and with the aim of supplying the already existing market. Therefore, the Group considered said acquisition as a merging of businesses.

To execute the operation, approval was obtained from the Competition German authorities.

The whole external financing was provided by Commerzbank in the framework of non-recourse transaction.

The list of the net assets acquired and the resulting consolidation negative difference follow:

- The consolidation negative difference arising from the transaction was entered under the heading of “Other operating income” of the Income Statement of the exercise.

In light of the calculation of the fair value of the acquired net asset, the Company went ahead and calculated the fair value of said businesses via cash flow discounts; said fair value is higher than the cost of the merging. In addition, said valuation was contrasted with the replacement value in use of an investment in plants of similar characteristics. Given that the value obtained in the calculation by cash flow discount was lower than the value of the replacement in use, the Management of the Group considered the least as the fair value of the businesses acquired and assigned said amount in its entirety as the greater value of the fixed property affected by business (Note 9).

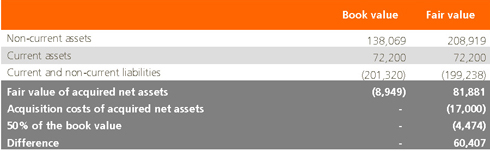

In calculating said fair value we employed the most conservative hypotheses for estimating the cash flows. Thus, the Management of the Group does not think there will are negative distortions in future cash flows. - On 24th September 2009, Biocarburantes de Castilla y León, S.A., a company, until then consolidated through the method of proportional integration, became consolidated through total integration when the remaining 50 percent of the shares held by third parties not connected to the Group were acquired for the amount of € 17M.

The company, Biocarburantes de Castilla y León S.A. was created at 50 percent each by Abengoa for the construction and operation of a two hundred million-litre bioethanol plant in Babilafuente (Salamanca), in operation since 2006.

This acquisition, which increases control over Abengoa’s capacity of ethanol production by one hundred million litres, is strategic from the R&D&i point of view since it puts Abengoa in control of the operations of the demonstration plant that produces ethanol from lignocellulosic biomass and which is the step prior to the industrial commercialization of the second generation technologies.

Ministerial Order ITC 287772008 dated 8th October, which develops the obligation to mix biofuels in fuels for use in transportation in Spain, establishes a minimum consumption objective of 5.83 percent of biofuels, with a minimum of 3.9 percent for bioethanol on the consumption of gasoline, which means a minimum consumption of 450 million litres of bioethanol, representing a 50 percent increase on the same minimum objective in 2008. The full integration of this plant, with the rest of the plants owned by Abengoa Bioenergía in Spain (Cartagena and Curtis-Teixeiro, Galicia) and Europe (Lacq and Rotterdam) would permit the obtaining of considerable logistic and operational synergies.

According to the above and pursuant to IFRS 3 on business combinations, the Administrators analyzed the assets and liabilities acquired and their subsequent assignment of their acquisition price for evaluation purposes, for which reason they considered the value of all the assets and liabilities, tangible and intangible, as well as contingent, as far as they may be objects of accounting recognition in accordance with the international accounting standards.

Thus, the assignment of the acquisition price entailed the consideration of all the factors taken into account when determining the acquisition price, the most important of which is the assignment of value (70.8 million Euros) to the non-current assets associated with the future exploitation of the bioethanol plant acknowledging in the Income Statement an added value in the amount of 24 million Euros for the excess between the cost of the business combination and the fair value of the net assets and liabilities acquired.

The main impacts on the Statement of Financial Position dated 31st December 2009 are as follows (in thousands of Euros):

From the difference shown in the chart above, € 24 M are registered in the Income Statement of the exercise for new acquisition and € 36 M directly against the equity for 50% of the stock shares that was held pursuant to IFRS 3.

Had it been part of the Group from 1st January 2009 onwards, the contribution of 50% of Biocarburantes de Castilla y León would not have amounted to a very significant variation with regards to the consolidated results after taxes for the 2009 exercise.

The incorporation of the rest of the subsidiary companies into the consolidation, in the 2009 exercise, did not amount to significant incidence on the overall consolidated figures of December 2009.