Annual Report 2009

- Legal and Financial Report

- 2009 Annual Consolidated Accounts

- Notes to the Consolidated Annual Accounts

- Note 9.- Financial Risk Management and Information on Financial Instruments

Note 9.- Financial Risk Management and Information on Financial Instruments

9.1. Financial risk

Abengoa’s activities are undertaken through its Business Units and are exposed to various financial risks: market risk (including exchange rate, interest risk and pricing risk), credit risk, liquidity risk and capital risk.

The risk management model attempts to minimise the potential adverse impact of such risks upon the financial profitability of the Group. Risk is managed by the Group’s corporate finance department, which is responsible for identifying and evaluating financial risks in conjunction with the Business Units operations, and quantifying such risks by project, region and company.

Internal written risk management policies exist for the overall management of risk, as well as for specific areas of risk such as foreign exchange, credit risk, interest rate risks, liquidity risk, and for the use of hedging instruments and derivatives and for the investment of surplus cash in hand.

In additional, there are official written management regulations regarding key controls and control procedures for each company, and the implementation of these controls is monitored through internal audit procedures.

The accounting policies regarding financial instruments are applied to the following:

a) Market risk

The Group activities fundamentally expose it to financial risk from foreign exchange, interest rates and changes in the prices of assets and commodities materials purchased (principally zinc, aluminium, grain, ethanol, sugar and gas). To cover such exposures, Abengoa uses options and swaps for exchange rate and interest rate contracts and futures contracts for the aforementioned mentioned products. The Group does not use derivatives for speculative purposes.

Foreign Exchange rate risks arise when the commercial transactions to be settled in the future, for which the assets and liabilities are not denominated in the functional currency of the entity.

To control foreign exchange risk, the Group purchases future currency sale/purchases options. Such contracts provide cover over the fair value of the future cash flows.

Approximately 95% of projected transactions which are not denominated in the functional currency of the Company are very likely highly transactions in regards to hedging account.

The main exchange rate exposure to the Group relates to the US Dollar, the Euro and the Brazilian Real.

Details of the financial hedging instruments and foreign currency payments as of 31 December 2009 are included in Note 11 of these Notes to the Financial Statements. The amount which is not covered is not significant.

The sensitivity of the fair values of the interest rate hedging derivative financial instruments against variations of 10% in currency exchange rates is not significant in the equity.

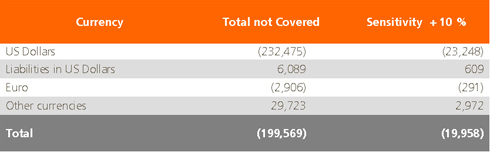

The following tables show a list of net assets and liabilities denominated in a currency which is not the denominated functional currency which is not covered by financial exchange rate hedging instruments, as well as the impact of a 10% movement in the exchange rate of the currencies:

The interest rates risks arise mainly from the financial liabilities at variable interest rates.

To control the interest rate risk, the Group primarily uses interest rate swaps and interest rate options (caps) which in exchange for a fee offer protection against a rise in interest rates.

A detail of the financial derivative instruments relating to interest rates as of 31 December 2009 is provided in Note 11 of these Notes to the Financial Statements.

The sensitivity of the fair values of the interest rate hedging derivative financial instruments against variations of 50 b.p. in market interest rates is not significant in the equity.

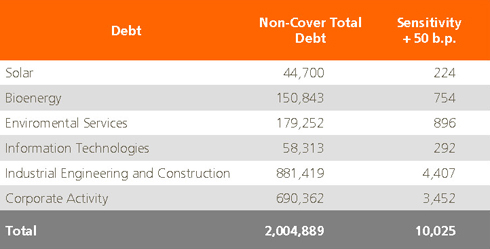

The following is a detail of financial debt with variable interest rates which are not covered by such interest rate hedges as well as the impact of a 50 basis point change in market interest rates:

The risk of a change in commodities prices arises through both the sale of products of the Group as well as in terms of purchasing commodities for production processes. In general, the Group uses future purchase contracts and options as listed on open markets, as well as OTC (over-the-counter) contracts with financial entities, to mitigate the risk of fluctuations in market prices.

A detail of the financial derivative instruments for commodities prices as of 31 December 2009 are detailed in Note 11 of these Notes to the Financial Statements.

The sensitivity upon reseves of a 10% change in the fair value of these instruments would be approximately € 4 M.

In addition, and independently to these transactions, during the past exercise, certain companies of the Group began engaging in buying and selling operations on the grain and ethanol markets, fully in accordance with management policy regarding trading transactions. These operations reflect the implementation of a strategy (approved by Purchasing Group Management) for the purchase and sale of futures and swap contracts in grain and ethanol, over which daily control and communications is exercised, as per the procedures set out in the aforementioned Transaction Policies. To mitigate the risk, the company establishes certain limits “stop loss” daily for each strategy taking into account the market in which they are going to operate, the financial instruments purchased, and the defined risks of the operation.

These operations are valued in the income statement on a monthly “mark to market” basis. During 2009, Abengoa has registered gains of € 1,999 thousand, of which € 1,630 thousand relates to gains on liquid operations and € 369 thousand are potential benefits based upon open contracts valued at the year end.

b) Credit risk

The main financial credit risk exposure is the failure of the third party to comply with their obligations within the transaction, being trade debtors and other accounts receivable, current financial investments and cash.

The majority of accounts receivable relate to clients operating in a range of industries and countries with contract which require ongoing payments as the development project advances, upon the rendering of services or upon completion and delivering of the project. It is normal practice that the company reserves the right to suspend the project if there is a notable breach in the terms of the contract, in particular the non-payment of amounts owed.

Additionally, prior to this stage, generally, the company relies upon the written confirmation of a first level for the purchase, without recourse, of accounts receivable (Factoring). In these arrangements, the company pays a fee to the bank to assume the credit risk as well as interest charges for the financing component. The company assumes in all cases that the accounts receivable are valid.

In this regard, derecognising of factored amounts receivable is taken only when all the requirements of IAS 39 are met to take of the assets of the balance sheet. That is to say, it is considered whether or not the risks and rewards inherent in the ownership of the financial asset have been transferred, including a comparison of the risk to the company before and after the transfer, considering the amounts and timing of net cash payments to be received. Once the risk to the grantor company is eliminated or is considered to be substantially reduced it is considered that the financial asset in fact has been transferred.

In general, for Abengoa, the greatest risk to such assets is the risk of not collecting a trade account receivable. This is because, a) it may be a significant value in the development of a works or in the provision of services; b) it is not within the control of the company. However, the risk of customers being unable to make a payment in such contracts is considered to be low, and typically relate to problems characterised as technical matters, it’s say relate to the own risk of the service rendered, which are within the control of the company. In either case, and to cover those contracts in which a risk could theoretically be identified, as a financial asset risk, the possibility of a delay in customer payment without the customer sighting trading causes, Abengoa states that, not only should it cover the risk of insolvency (or bankruptcy) right but also the fact or noted insolvency (as a result of a decision by the customer’s treasury own management without resulting in "a general moratorium”). As such, and if the individual evaluation, as performed for each contract, concludes that the related risk to the contract has been passed to the financial entity, the account receivable is removed from the balance sheet at the time of passing the risks to the financial entity, as per IAS 39.20.

As indicated, it is Abengoa’s policy to transfer the credit risk associated with customers and other accounts receivable through the use of non-recourse factoring. As such, with regards to considering risks inherent within debtors and other accounts receivable on the balance sheet, amounts should potentially be excluded relating to works completed awaiting certification for which Factoring contracts are in place, as well as amounts which could be factored which are outstanding to be submitted to the financial entity providing the Factoring and also those debtors included which are covered by an insurance policy. As such, under this policy, Abengoa minimises its exposure to credit risk.

A debtors ageing analysis as of 31 December 2009 is included within Note 12 of these Notes to the Financial Statements. The same Note also includes an analysis of movements in debtor provisions over the year.

c) Liquidity risk

The liquidity and financing policy of Abengoa has the objective of assuring that the company maintains sufficient funds available so as to meet its financial obligations as they fall due. Abengoa uses as its main sources of financing:

- Non-recourse Project financing, which typically is used to finance any significant investment (see Notes 2.4 and 15). The repayment profile of each project is established on the basis of projected cash generation of the entity in question, with a considerable range varying depending upon the visibility of future cash flows of each company or project. This ensures that sufficient financing is available with terms of repayment which mitigate to a significant extent the liquidity risk.

- Corporate Finance, used to finance the activities of the remaining companies which are not financed under the aforementioned financing model. This means of financing is managed through Abengoa S.A., which pools cash held by the rest of the companies so as to be able to re-distribute funds following the needs of the Group (see Notes 2.18 and 16).

To ensure there are sufficient funds available for the repayment of debt with respect to its capacity to generate cash, Abengoa has put in place the following criteria and actions:

1) Maintaining sufficient leverage headroom by not exceeding a given Net Debt/EBITDA ratio limit of corporate financing. The maximum headroom as per the financing contracts in 2009 and 2008 was 3,0 and 3.25, respectively. Net debt is calculated as all third party borrowings less cash and financial investments of current asset excluding the debt of operations financed without recourse. The denominator of the ratio is derived as the EBITDA of the entities which do not utilise non-recourse project finance and incorporating R&D&i expenses for the exercise.

At the close of the 2009 and 2008 exercises, Abengoa fulfils the requirement related to said financial ratio.

2) Each year a financial plan is prepared and approved by the Board of Directors which encompasses all financing requirements and the way by which those will be covered. The plan is prepared in close collaboration with the Corporate Finance Department and various Business Units.

3) Ensuring the ability to meet financial obligations in the coming months. In this regard, in 2009 Abengoa Corporate Finance completed two operations through the issuance of bonds for the total amount of € 500 M.

In accordance with the above, there is a diversification in the sources of finance, in the attempt to prevent concentrations that may affect the risk of working capital liquidity.

.

Management reviews the Group’s liquidity reserves (made up of the availability of credit (Note 16) and cash or cash equivalents (Note 13) in comparison to the anticipated cash flows.

The Group utilises factoring without recourse lines, contracted to finance normal business activities for € 1,800 M available as at the end of the financial period € 715 M. Besides, the Group has working capital overdraft facilities, from which € 7,574 thousand available from a total of € 170,550 thousand.

An analysis of financial liabilities of the Group shown by period until due, being the remaining time between the balance sheet date and the date of maturity of the various debt instruments, is included within the following table:

d) Capital risk

The Group manages its investments in capital to ensure that its subsidiaries are secure in terms of their continued activity from the point of view of their equity statement through maximising the return to the shareholders by optimising the structuring of the equity and third party debt financing on the entities balance sheets.

Capital management is undertaken by the Group strategy, whose focus is to increase the value of the business in the long term for both shareholders and investors, as well as for employees and customers. The objective is the attainment on an ongoing and sustained basis of the Group’s results through organic growth. To achieve these objectives, it is necessary to strike the correct balance between, on one hand, control over the financial risks of the businesses, and on the other, financial flexibility required to achieve those objectives.

9.2. Information on financial instruments

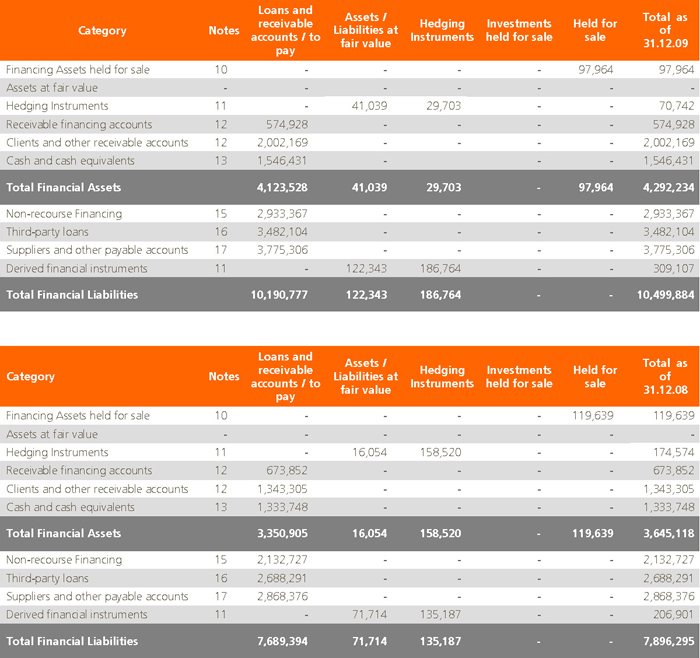

a) The financial instruments of the Group are primarily deposits, debtors and amounts receivable, derivatives and loans. Financial instruments analysed by balance sheet category are as follows:

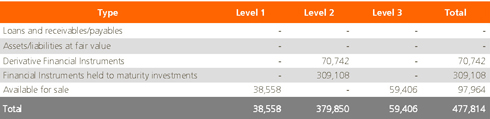

b) On 1st January the group adopted the modification to IFRS 7 for Financial Instruments priced at fair value, which requires a breakdown of the fair value measurements based on the following classifications:

- Level 1: Assets or liabilities traded on the active market.

- Level 2: Valued based on prices on observable but not traded markets, whether based on direct prices or through the application of valuation models.

- Level 3: Valued based on non-observable market data.

Below is the detail of the assets and liabilities of the group at fair value at the close of the 2009 exercise (with the exception of those assets and liabilities with book values that are close to fair value, non-traded equity instruments valued at their costs and contracts with components that cannot be reliably evaluated):

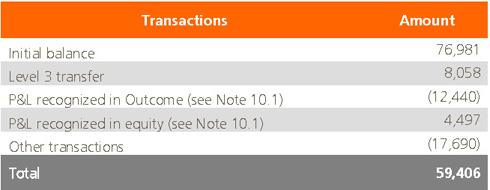

Below is a detail of the changes in the fair value of level 3 assets and liabilities at the close of the 2009 exercise: