Annual Report 2009

- Corporate Social Responsibility Report

- Greenhouse Gas Emission Inventory

- Inventory Generation and Maintenance Standard

Historically, Abengoa has demonstrated its firm commitment to the environment. Consequently, the aspects of sustainability have always been taken into consideration in the activities conducted by the Company. In 2007, under the direction of the Chairman’s office, a work group consisting of a team from the Abengoa Quality and the Environment Department and by business unit coordinators was set up with the purpose of developing a standard for generating and maintaining Abengoa’s greenhouse gas emissions inventory (Common Management Systems Standard).

Photo taken by Joséé Alejandro Aviléés Flores, from Telvent, to the 1st Edition of the Abengoa Sustainability Photography Contest

As a product of this effort, NOC-05/003 was published in June 2008. The aim of this internal norm is to define the methodology for the generation and maintenance of an emissions inventory to enable monitoring and reporting of greenhouse gas emissions in all Abengoa companies. This inventory includes both direct and indirect emissions.

There are very few companies with robust methodologies for quantification of their Scope 3 emissions. Considered to be best practice, Abengoa has incorporated into its standard the methodology for calculating these Scope 3 emissions by integrating the entire chain of suppliers of goods and services.

Scope

NOC-05/003 applies to all Abengoa companies governed by the Common Management Systems. It is also applicable to JVs, EIGs and other consortiums or concession companies in which an Abengoa company has control of management.

For purposes of the inventory, the following activity segments have been established: production, execution of works and maintenance, offices, factories and workshops, warehouses, and transportation.

Each company’s inventory includes both direct and indirect emissions. In other words, the emissions associated with sources under the control of the company (Scope 1 of the Kyoto Protocol), emissions associated with the generation of the acquired electrical power and thermal energy consumed (Scope 2), emissions deriving from the chain of value of acquired energy consumed, losses in the transmission and distribution of acquired energy consumed, emissions resulting from acquired goods and services, emissions associated with business trips, and emissions linked to commutes to the work place (Scope 3). Direct CO2 emissions from biomass combustion or transformation covered under the inventory are reported separately.

The GHGs listed in the inventory are the gases included under the Kyoto Protocol: carbon dioxide, methane, nitrous oxide, hydrofluorocarbons, perfluorocarbons, and sulfur hexafluoride.

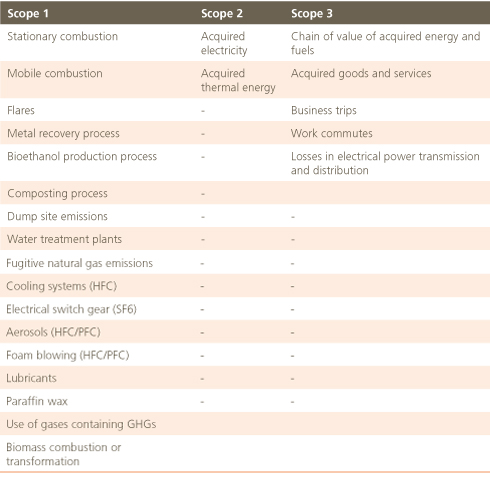

Main Emission Sources

To facilitate and standardize GHG emission computation, the NOC includes in-depth methodology for calculating the emissions of the three Kyoto Protocol scopes. The main sources taken into consideration are those shown below:

Bases for Calculating Emissions

Emissions can be determined by applying a methodology based on either calculation or metering. The former is the chief methodology for determining emissions, and the latter is restricted to determining channelized emissions.

It is important to point out the bases for calculating the emissions corresponding to acquired goods and services (Scope 3). All purchase orders include the obligation of the supplier to provide details on the emissions associated with the requested goods or services. Suppliers are also under the obligation to sign up in writing to the Social Responsibility Code for Abengoa suppliers and subcontractors. In order to facilitate the adaptation of all suppliers to the new purchasing conditions a transition period has been established for those who are not immediately in a position to submit their emission details, but who undertake in writing to implement an emissions reporting system. The duration of the transition period is six months. Suppliers who do not report their emissions or do not commit to implementing a reporting system within this time period are excluded, with the exception of exclusions processed via NOC authorization, with companies being responsible for estimating the significant emissions of the goods or services provided in these cases.

Given that the inventory is in the process of being implemented among company suppliers, in calculating Abengoa’s 2009 GHG inventory, there was an exceptional allowance provided for the estimation of emissions associated with products or services (Scope 3) from suppliers who were not able to report their emissions immediately. Estimations in these cases were made by Abengoa companies according to emission factors and the databases of internationally recognized sources and bodies. Thus, approximately 50% of the Scope 3 supply chain emissions were estimated directly by Abengoa in the 2009 Abengoa GHG inventory.

The NOC establishes that each piece of emission data be accompanied by a quality index. This quality index is associated with the emissions data for each source and greenhouse gas, as well as each parameter involved in the calculation. This quality index shows the degree of reliability of the data and is always expressed with a standardization basis of 10.

Minimum quality requirements are established under this standard for each emission source, according to the emitting potential of the center and whether it is a main, secondary or minimal source.

Recording and Reporting Information

At present, the companies are reporting their emissions by means of the corporate reporting system, which contains a GHG emissions section that is accessible to the persons in charge of the inventory. This section enables access to the monthly GHG emissions report of each company (Scope 1, 2 and 3 details) and to the list of suppliers and their degree of commitment to the NOC (provision-related emission inputs).

Abengoa is in the process of completing the implementation of a computer application that has been specifically designed to calculate GHG emissions and which will also enable data consolidation and enhanced inventory functionality.

Attributing Emissions to Products and Services

The NOC covers future attribution of emissions to products. This allocation shall be performed through the methodology for main and auxiliary emissions distribution centers, which is similar to that of cost centers. GHG emissions were not attributed to products or services in the 2009 inventory.

Defined Control Tools

The NOC establishes the obligation of all Abengoa companies to implement an internal auditing process in order to verify proper execution of the requirements included under this standard.

This auditing process planning must be thoroughly documented on an annual basis.

Furthermore, each company’s inventory is subject to evaluation within the control and monitoring visit program managed by Abengoa’s Department of Quality and the Environment.

Photo taken by José Ángel Molina Reyes, from Inabensa, to the 1st Edition of the Abengoa Sustainability Photography Contest

Implementation Methodology

During the second half of 2008, Abengoa companies implemented the emissions inventory by applying these stages:

- Selection of the emissions quantification methodology

- Data compilation

- Methodology application

- Reporting

With the ultimate aim of ensuring proper implementation of the NOC in all of the group companies, Abengoa conducted training/feedback sessions for first- and second-level managers (approximately 1,000 people). In 2009, Abengoa proceeded to consolidate 2008 emissions from the different companies.