This website uses third-party cookies to collect statistical information related to your navigation. If you continue to browse, we consider you accept this use. See more information on our cookies policy here.

Annual Report 2011

- Corporate Social Responsibility

- Independent Panel of Experts on Sustainable Development (IPESD)

- Questions of the IPESD on the 2010 CSR Report

GHG management

1. We welcome the inclusion of all operating entities in the capture of GHG emissions data.

- In order to understand the evolution of GHG emissions, can Abengoa disclose the historical trends and the breakdown of GHG emissions by activity and explain any major change in the trends?

- Furthermore, can Abengoa include targets established as this would increase the transparency of Abengoa’s commitments and help explain and align the actions undertaken in relation to those commitments?

In 2008, Abengoa implemented the Abengoa greenhouse gas (GHG) emissions inventory, which in addition to recording the direct and indirect emissions of all companies that make up the corporation, takes into account emissions derived from third party-acquired products and services.

At present only the 2009 and 2010 annual inventories have been verified by a third party and disclosed externally. Given such a short history, it is not yet possible to have a clear picture of how the company’s GHG emissions have evolved over time.

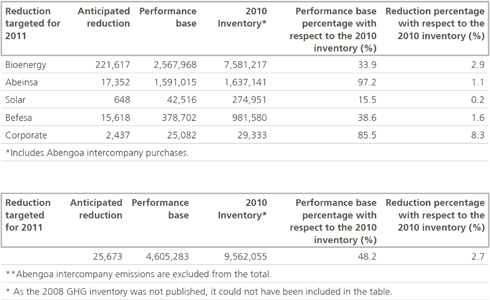

Below is a summary chart which shows anticipated reductions for the year 2011 over the 2010 GHG inventory by business group and consolidated total:

Renewables

2. Abengoa generates significant revenues from energy markets that are subsidized by governments. However, in the last year there have been important changes in regulation and support mechanisms (mainly feed-in tariffs) of renewable energies in Spain and in other countries.

- Does Abengoa see any specific obligation to society that arises from the use of public subsidies and could Abengoa explain the impact of the changes in the different support mechanisms from renewables across the relevant countries of operation on its sustainability strategy and specific renewable targets?

Public support in the form of subsidies entails a duty for organizations to enhance social well-being. In the case of renewable energies, Abengoa is making a significant contribution to help the range of subsidized technologies ascend up the learning curve, thus improving efficiency and lowering costs so that these technologies may become competitive on their own in the energy market as soon as possible. In the particular case of second-generation biofuels, this reduction in production costs would not have been possible without Spanish or European energy policy.

Furthermore, the technology being developed by Abengoa to generate power using renewable sources involves numerous benefits for society from an economic, geopolitical and environmental standpoint.

The development of renewable alternatives also helps to halt climate change as the result of the reduction in greenhouse gas emissions. This plays a decisive role in enhancing people’s quality of life by decreasing the number of health risks, lowering environmental impact, and driving down economic costs.

In the specific case of solar power, over the last years, we have received public support, for example in the form of R&D grants and feed-in tariffs. This support has helped us to develop cutting-edge solar technologies, especially in the area of Concentrating Solar Power (CSP), and to build commercial plants in Spain, the USA, and other markets.

Public support has helped the CSP industry to take the first steps towards a full-scale energy transition, in which our economies depend less on petroleum and nuclear energy but on electricity generated from renewable sources. Abengoa aims to continue driving that change by developing and rolling out new solar technologies that are technologically mature and economically viable within the next few years. Abengoa is investing heavily in R&D and has a clearly defined technology roadmap to reduce the cost of CSP significantly over the coming years. Putting to use Abengoa’s own resources as well as public funds, we aim to be competitive with conventional energy sources by 2020.

In our experience, there are different regulatory frameworks, such as Feed-in Tariffs in Spain or Federal Loan Guarantees in combination with Renewable Portfolio Standards in the USA, that have proven their capacity to trigger the development of CSP projects and make them economically viable, while serving their purpose of creating value to society.

In the US, the Obama administration has signalled their intention to continue supporting the roll-out of renewable energy sources. With the presidential elections later this year, we do not expect any concrete measures in the immediate future. In Spain, the new government has announced the continuation of the Feed-in Tariff scheme for CSP projects that are currently included in the pre-assignation registry. At the same time, the government announced a moratorium on new renewable energy projects while conducting an in-debth review of Spain’s energy policies. This review process may take some time. In any case, the government also announced that it stands by Spain’s National Renewable Energy Plan of November 2011, which states the objective to install a total of 4.8 GW of CSP in Spain until 2020. This implies the need to install approximately 2.4 GW of additional CSP capacity beyond the plants currently included in the pre-assigned registry.

In view of all these developments, our objective to reduce the cost of renewable energy over the coming years in order to become competitive with current traditional energy sources will continue to be the cornerstone of our strategy.

- Has Abengoa managed to reduce the cost of deployment of its renewable technologies as a result of public support policies and its own R&D efforts, thus facilitating a widespread and scaled-up deployment in developing countries?

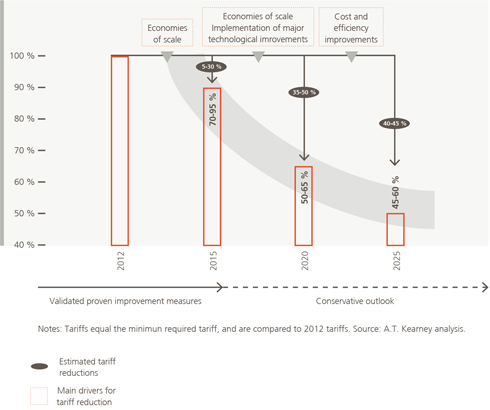

In the case of Solar power, Abengoa has successfully reduced the cost of CSP over the last years and will continue to do so in the future. The European Solar Thermal Electricity Association (ESTELA) report illustrates the important technological progress of the sector. Abengoa has participated in this study and shares its conclusions, summarized in Figure 3 below.

In the case of bioethanol, this liquid fuel is commoditized and its price is determined by the market forces. Public regulation has helped to create a market and to develop more efficient second-generation technologies like biomass-based ethanol.

Biodiversity

- 3. Abengoa describes in its CSR report a systematic process for managing the biodiversity impacts of its activities, the Environmental Sustainability Indicator

(ESI) system. - Can the company provide more information about how many projects/contracts have been rejected due to the ESI screening process and what is the proportion of rejected projects to the total number screened?

The Environmental Sustainability Indicators (ESI) constitute an environmental management system that was devised to monitor, compare, report on and set improvement targets for Abengoa facilities. This environmental management system is not a mechanism for prior assessment of environmental impact and is therefore not geared towards analyzing and determining a project’s environmental viability.

Pre-project environmental impact analysis processes are carried out in accordance with existing legal requirements and specific regulatory procedures designed for this purpose.

Therefore, once the environmental viability of a project has been verified, the ESIs enable us to increase facility sustainability and accomplish objectives that are more demanding than those covered under environmental regulations.

In line with this approach and based on this environmental viability analysis, no project is actually rejected, but rather modified in relation to the initial design or developed through measures approved by the management, such as impact compensation initiatives.

- 4. Engineering, construction and energy companies can cause large impacts on the surrounding environment and communities.

- Please describe how Abengoa mitigates the social and environmental impacts of construction works and in particular how it mitigates the impact of waste (in particular hazardous waste) created by operations..

Abengoa has implemented a variety of initiatives to mitigate the environmental and social impacts of its activity. Fundamentally, environmental impacts are mitigated through the environmental management systems in place at all Abengoa companies and, specifically, by means of the GHG inventory and the ESI indicators.

As far as the social dimension is concerned, impacts that may be generated by projects are mitigated through community dialog and specific actions aimed at addressing citizens’ expectations, including project information campaigns and open house events. Thus, as in previous years, in 2011 the Solúcar Solar Complex, located in Sanlúcar la Mayor, Seville, held informative open house events for local community members. In addition, Abengoa facility risk analysis was implemented over the year through a pilot project consisting of carrying out risk assessments in four of the company’s most significant facilities in order to determine procedure improvement areas based on the results obtained. Following procedure rectification, the questionnaire will be deployed among the other facilities. This will enable us to detect and mitigate social, environmental and economic risks and to identify endorsers and establish mechanisms for dialog with endorsers.

With the aim of mitigating the impacts of wastes generated during operations, Abengoa takes action through a specific management process based on operational control of activities, designed in keeping with an environmental management system in accordance with the 14001 Standard and approved by an external entity.

In accordance with our Environmental Management Policy, all companies that generate hazardous waste carry out an exhaustive process of identifying and tracking transport of these types of wastes to government-authorized agents, regardless of whether they belong to Abengoa or to outside companies.

In relation to our construction business, Abengoa subsidiaries have a raft of waste management procedures in place that establish the standards for managing the waste generated by the company and its subcontractors. One example of these types of practices is the construction waste management plan for the Helioenergy I CSP plant, which includes definitions, identification and management systems that apply to wastes, transfer treatment and duties.

Monitoring and control documents likewise enable the identification of each waste allotment, the authorized carrier, and final destination in delivery to a government-authorized agent in accordance with Spanish and European regulations.

- What have been the most significant incidents related to these wastes and how have they been managed?

The most significant incident relating to waste management occurred in 2001 in the Spanish region of Murcia and involved a boiler explosion at Trademed, a company specializing in the treatment and deposit of industrial waste. At that time, however, the company was yet to be integrated within Befesa Gestión de Residuos Industriales and was, therefore, under Abengoa management.

To avoid more incidents of this kind in the future, the following steps were taken:

- Construction of drum storage facilities, all fitted with the corresponding security and safety systems.

- Paving of transit zones and implementation of rainwater channeling and collection systems across these zones. Modernization of the waste treatment and inertization zone, thus equipping the facilities with cutting-edge infrastructure geared towards excellence in waste treatment, focusing on minimization, reuse and valorization before final disposal (such as by fitting grinding mills for empty drums and containers so that they can subsequently be valorized).

Similarly, Befesa Gestión de Residuos Industriales conducts continuous assessments of compliance to environment law and regulations in accordance with the environmental management system.

As a result of this effort, Abengoa has not received any reports of any incidents taking place since the incident occurring in the area.

- Are there any synergies with Abengoa’s waste management business?

Generally speaking, there is no reason for these synergies to arise. At Abengoa there are two potential cases at present:

- Companies whose activity generates wastes that serve as raw material inputs for a process of another Abengoa company.

- Companies whose activity generates wastes that are identified and treated by third parties without necessarily being managed by any of our companies.

Management of our own waste accounts for only a very small percent of group business, making it practically impossible to obtain synergies from this process. Most of our knowledge is obtained from Abengoa subsidiaries that manage the waste of external third parties and, at the moment, we cannot harness this within our own management processes as we do not generate the kinds of waste we are specialized in, meaning those that make up core waste management business at Abengoa.

5. As each Abengoa company already has a management system which assesses lifecycle phases of products, the report could benefit from more detail on the results.

Broadly, how does Abengoa monitor and report the life-cycle and eco-efficiency of its products, and what are the company’s long-term intentions on reporting??

Assessment of the eco-efficiency of Abengoa products and services is a project that is currently at the preliminary stage. Over the course of 2011 Abengoa finished developing the methodologies needed to calculate the carbon footprint of its major products and services, based primarily on the GHG Protocol Product Life Cycle Analysis and PAS 2050 and, where applicable, on use of the Product Category Rules (PCR).

The companies have therefore been prepared to proceed to calculation of the carbon footprint of their products and services, with this being a process they will carry out in 2012 based on the 2011 GHG inventory.

The following are listed below as examples of methodologies:

- Solar energy: calculation will be made of the carbon footprint related to thermoelectric (CSP kWh produced by either a central receiver or by a parabolic trough station) and photovoltaic (photovoltaic kWh produced through conventional silicon cells and dual-axis tracking) power.

- Desalinated water: using data from the Befesa desalinating plant in Skikda, the methodology has been developed to calculate the carbon footprint of a cubic meter of desalinated water..

- Zinc recovery process: for which information from one of our zinc recycling plants in which purified Waelz oxide is obtained was used to label this product as a by-product and supplementary service. Under this methodology the ferrosite (slag commercialized as a byproduct for use as a building material) and waste management activity resulting from the process were taken into account.

Human Resources

6. It is our understanding that in 2010 Abengoa completed implementation of the internal standard, Social Responsibility Management System (SRMS) based on SA8000, across its significant operations.

What are the major actions Abengoa has undertaken as a result of implementation, and what are Abengoa’s intentions on reporting the results from its internal audit?

In keeping with the social responsibility commitments acquired through adherence to the United Nations Global Compact and those deriving from the company’s own Code of Conduct, Abengoa has undertaken a policy on labor-related social responsibility consisting of the integration of a management system inspired by the international SA8000 model, which assures ongoing improvement in the company’s social performance.

While Abengoa has not established deadlines for Abengoa companies to become certified, to date three companies have already done so. Furthermore, the company has taken the standard’s management model as a reference for application throughout the company.

Along these lines, committees on labor-related social responsibility have been set up in all groups, companies, and business units.

- Differences in local salary levels are significant – what are Abengoa’s policies which direct this, and how does this relate to the SA 8000 standards on remuneration

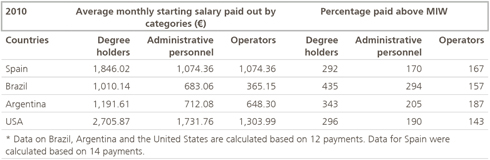

At Abengoa salary categories in each country surpass the MIW and therefore, in line with the specifications of the SA8000 Standard, the company’s remuneration policy ensures that all employees are able to meet basic needs and allows for a certain degree of discretionary expenditure capacity.

The table below, published in the 2010 CSRR, shows the percentage difference between Abengoa’s standard starting salary and local minimum inter-professional wage (MIW), taking different professional categories into account.

Supply chain

7. Please describe the process followed by Abengoa to assure supplier compliance with its sustainability policies.

- How many suppliers does Abengoa consider could pose a risk to Abengoa’s sustainability, how many of those suppliers have been audited for compliance, and what have been the results (total number and proportions disqualified, placed onto an improvement program, and found to be compliant, respectively)?

- How many of those audits were conducted by independent assessors?

As part of Abengoa’s unwavering commitment to sustainability, it is essential for the company to be able to rely on providers who embrace this commitment and undertake to uphold sustainability. Therefore, since 2008 Abengoa requires that all company suppliers sign up to the Abengoa Social Responsibility Code (SRC) based on the principles of the Global Compact and inspired by the SA8000 Standard, which includes commitment in complying with and promoting social, environmental and ethical aspects.

In 2010, suppliers signed 3,862 agreements with Abengoa companies; in 2009 this figure was 7,596, and in 2008, 5,299. This amounts to a total of 16,757 signed agreements as of December 31, 2010.

In addition, since 2008 Abengoa has been requesting the information needed from all company providers in order to determine the Greenhouse Gas (GHG) emissions linked to their production processes. This information enables the company to undertake the process of lowering the emissions associated with raw material inputs by selecting suppliers whose production processes are more sustainable.

In 2011 we embarked on the development of a responsible purchasing system which will enable us to ascertain the number of suppliers who may pose a sustainability-related risk to the company. Four main phases have been identified during this process:

1. Preliminary purchasing system diagnostic

2. Supplier analysis

3. Supplier auditing

4. Sustainability-based supplier assessment or rating

Implementation of the first two phases required collaboration among the purchasing departments of the different Abengoa companies in order to select various assessment criteria allowing for the particular characteristics of each company activity to be taken into account.

In carrying out supplier analysis, variables including supplier country of location, supply nature, degree of visibility with respect to customers or the media, solvency risk, etc. were evaluated.

The supplier auditing model is intended to determine the degree to which Abengoa providers ensure compliance with the principles specified in the Abengoa Social Responsibility Code. Audits will be defined according to the supplier’s degree of criticality, obtained during analysis (Phase 2), and will be carried out through self-assessment questionnaires, offsite audits or onsite audits in which visits will be made to supplier facilities, for which it remains to be determined whether this process will be handled by an independent third party or by a multidisciplinary Abengoa team.

A committee of Abengoa purchasing managers has also been set up in order to oversee smooth operation of the model, establish objectives to be achieved, and analyze the results obtained from the audits.

Through this procedure, Abengoa seeks to engage its providers in the commitment to corporate social responsibility and sustainability by conveying corporate values to the supply chain, forestalling any conduct that may contravene our principles of performance, and rewarding the excellence of our suppliers and providers.

At the end of 2010, the Focus-Abengoa Foundation introduced the Sustainable Business Awards created to publicly acknowledge Abengoa suppliers who have made an active contribution to sustainability through their performance and set an example for other organizations. The award ceremony for the first edition was held in June 2011 and prizes were presented to Novozymes and Sulzer AG in the Large Company category and to Aislamientos Desmontables in the SME category.

Materiality

8. The complex matrix diagram and the large number of issues listed as significant in the CSR report make it difficult to understand the process whereby Abengoa determines which are the most material items for inclusion in the report.

- Could Abengoa explain which were the key stakeholders it consulted and which top five issues they identified?

- Similarly, which top five issues were identified through internal consultation processes?

- If these top externally and internally identified issues had been plotted on the materiality matrix diagram, what result would have emerged?

The contents published in the 2010 Corporate Social Responsibility Report (CSRR) cover aspects and indicators reflecting the significant social, environmental and economic impacts of the company or those that may have a substantial influence on stakeholder assessments and decisions according to the results of the process of analyzing relevant matters carried out by Abengoa at the end of 2010.

The procedure for selecting relevant CSR matters which is centered on two bases for analysis that subsequently intersect to obtain the final result:

- external factors, related to the expectations of Abengoa’s stakeholders and the importance they attach to the different matters; and

- internal factors, which determine the significance of the different issues for the business, company management and, ultimately, in meeting objectives that form part of business strategy.

The following were analyzed in preparing the list of external factors:

- International reporting standards, consisting primarily of the GRI and the AA1000 AS (2008).

- Chief competitors and comparable companies, both national and international.

- Socially responsible investors. The analysis of indexes such as the DJSI and the FTSE4Good helps to determine which matters are significant for investors and shareholders.

- International initiatives, including the United Nations Global Compact and Caring for Climate.

- Reader response to last year’s report, obtained through the communication channels made available for this purpose.

- Periodic review of applicable law.

- The media. Through the analysis of Abengoa’s media presence and that of other companies in the industry, the positive and negative CSR-related issues receiving the most attention from the media were identified.

In preparing the list of internal factors, the results of similar procedures conducted within the different Abengoa businesses were analyzed, and a committee composed of Abengoa employees and managers was set up, representing all company sectors and activities.

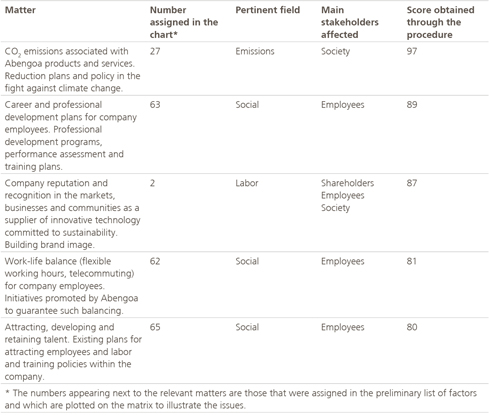

The five issues that received the highest score among the matters determined to be relevant were the following:

The five issues are illustrated below:

The five external factors deemed to be of most relevance were the following:

1. Reputation and recognition

2. Attracting, developing, and retaining talent

3. Creating jobs

4. Work-life balance

5. CO2 emissions

And the five internal factors considered to be most relevant were the following:

1. Work-life balance

2. Company career plan and professional development

3. Promoting diversity and equality between men and women

4. Lack of women in executive positions at corporate level and across business groups

5. Working environment and employee satisfaction surveys

Governance

9. What action does Abengoa take to protect the interests of minority shareholders, besides complying with Spanish capital market laws?

As an example, could Abengoa explain how the recent private placement of Class B shares was valued and how minority shareholders’ investments in Abengoa were

protected? Were they consulted on the transaction?

In addition to complying with legal requirements pertaining to shareholder reporting, Abengoa has implemented specific communication channels, such as the Shareholder’s

Electronic Forum, through which shareholders, be they minority or not, may request from administrators any information or clarifications they find necessary regarding issues included in the agenda of the General Shareholders’ Meeting or formulate any questions they consider to be of relevance in writing for submission thereof up until the seventh day before the scheduled Shareholdings’ Meeting.

Shareholders may also verbally request information or clarifications regarding matters on the agenda during the Shareholders’ Meeting and, in the event that it is not possible to fulfill the shareholder’s right at that time, administrators are obligated to provide such information in writing within seven days after the conclusion of the Shareholders’ Meeting.

In addition, Abengoa maintains ongoing contact with company shareholders through its Web site, where shareholders are provided with an email address they can use to transmit all types of queries to the company.

Abengoa’s General Shareholders’ Meeting held on April 10, 2011 approved modification of the company bylaws with the aim of including potential creation of Class B shares. This agreement was approved by a majority of over 90% of current social capital. Furthermore, in the interest of protecting the interests of minority shareholders, the investment agreement reached with the First Reserve Corporation, by means of which the U.S. investment fund specializing in energy sector investments purchased an equity interest in Abengoa through the subscription of Class B shares, received a favorable report from the Board of Directors of Abengoa, S.A. and underwent prior assessment by means of the report issued by KPMG, S.L. as the independent external auditor differing from the company’s accounts auditor designated by the Mercantile Registrar.

The transaction approved by resolution of the Board of Directors (which has power of issuance, delegated expressly by the General Shareholders Meeting held on April 10, 2011) does not require proactive consultation with minority shareholders due to being a transaction carried out with a qualified investor. Minority shareholder interests are nevertheless protected by the presence of independent officers on the Board. Pursuant to regulations pertaining to the securities market, the Board comprises a sufficient number of recommended independent officers to perform their duty: that of protecting the interests of shareholders without being conditioned by relationships with the company, its significant shareholders or company directors.

In short, with respect to the transaction involving placement of Class B shares, minority shareholder interests were safeguardedthrough approval of the transaction by agreement of the Board of Directors and by means of favorable reports from the Board itself as well as the auditor.

Anti-Corruption Policies

10. The CSR reporting complies with the GRI criteria, but we would suggest benchmarking this reporting against the UNGC/TI 10th Principle Reporting Guidelines which call for a more complete account of anti-corruption policies and how they are implemented and monitored. Abengoa reports that there were no instances of corruption in 2010.

- Can the company explain how it applies a zero tolerance policy in difficult countries where it has substantial business in Latin America, Africa and Asia and how it deals with solicitation for small and larger bribes in such environments?

Abengoa, which signed up to the Global Compact in 2002, upholds each one of the ten principles, and strives for complete integration of these principles into the strategy and policies governing the company’s day-to-day operation. With regard to Principle 10: “businesses should work against corruption in all its forms, including extortion and bribery”, the company has different procedures in place that are intended to prevent all types of corruption within the company.

Abengoa has developed an internal approval system which ensures that all contracts comply with the U.S. Foreign Corrupt Practices Act (FCPA). The Internal Risk Control Procedure likewise makes sure that the individual who authorizes payments is different from the person who manages a contract. As a further guarantee, since 2007 Abengoa voluntarily submits its Internal Control Systems to external evaluation by means of the issuance of an audit opinion in keeping with PCAOB standards and compliance auditing specified in Section 404 of the Sarbanes-Oxley (SOX) Act.

In addition, all Abengoa employees have an obligation to know, understand and abide by laws and regulations, along with the provisions of Abengoa’s Code of Conduct and other policies, that apply to conducting business. In the event that a national, state or local agency has adopted a more stringent policy than Abengoa’s policy regarding gifts and gratuities, the company’s employees and representatives must adhere to this more stringent policy.

In this regard, the U.S. Foreign Corrupt Practices Act (FCPA) makes it a crime for companies and their officers, directors, employees, and agents to pay, promise, offer or authorize the payment of anything of value to a foreign official, foreign political party or officials of public international organizations for the purpose of obtaining or retaining business. Payments of this nature strictly contravene Abengoa’s policy even if the refusal to make them may cause Abengoa to lose a business opportunity. For this reason, Abengoa upholds this law and ensures due compliance by incorporating into its Code of Conduct, known by all employees and published on the corporate Web site, the aforementioned prohibitions.

The company also has a specific communication channel with management and governing bodies in place for employees and any other interested parties to serve as an instrument for raising any issues that may involve instances of irregularity, non-compliance or conduct which contravenes ethics, legality and norms governing Abengoa operations and in compliance with the Sarbanes-Oxley Act. There were no corruption-related incidents recorded through these information channels at Abengoa in 2010.

© 2011 Abengoa. All rights reserved